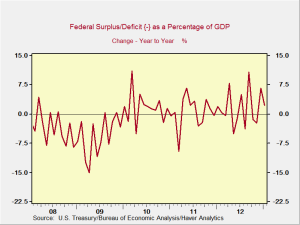

The deficit has dropped off the radar for a bit, what with the agreement to postpone debate about the debt ceiling and the generally improving economy, but recent events make it a good idea to check in and see where we are.

April 30, 2013

The deficit has dropped off the radar for a bit, what with the agreement to postpone debate about the debt ceiling and the generally improving economy, but recent events make it a good idea to check in and see where we are.

April 3, 2013

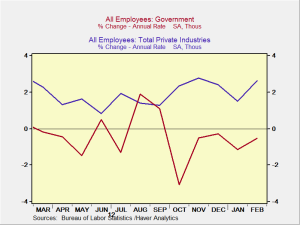

For the past couple of years, we’ve seen a strong first quarter followed by a much weaker second quarter. Initial signs suggest that the pattern may continue this year as well. Should we expect that—and, if so, what would it mean?

First, the good news: the first quarter was very strong. Economists are estimating that growth could have been as strong as 3 percent, which is well above expectations. Private employment continued to grow, with signs of an increasing growth rate over the past year, while government employment recovered somewhat after a tough fourth quarter, as shown in the chart below.

March 4, 2013

Despite the dire warnings, the sun rose today and people went to work. Planning shifted, if it hadn’t already, from avoiding the sequester’s spending cuts to implementing them. Entrepreneurs launched t-shirts and tchotchkes based the sequester and furlough.

Politicians, who had been warning of the disastrous consequences of the spending cuts, haven’t exactly backed off. Instead, they’ve adjusted the time frame—much like the doctor who had given his patient six months to live but then granted him an extension when he couldn’t pay off the bill during that time.

February 21, 2013

The markets have had a good run for the past six weeks, with a return through Tuesday of more than 7 percent for the S&P 500 Index. The run seemed to have been predicated on the fiscal cliff deal at the end of last year, the impression that the Federal Reserve (Fed) would continue to support the economy with low interest rates, the resolution of the European debt crisis, growing corporate earnings and profits, and a real economy in steady recovery. Retail investors had started pouring money back into equities, and there was talk of a “Great Rotation” out of fixed income and back into stocks.

Well, the real economy is still in recovery, but the other pieces of the puzzle are looking ragged. Yesterday, the Fed published minutes from the most recent meeting of the Federal Open Market Committee, showing that the committee is not unified in its decision to maintain purchases of Treasury and mortgage securities. This raises the possibility that rates might increase much sooner than the market had thought. Sequestration has also moved back to the front pages of the major papers, suggesting that the political risk from Washington is rising. In addition, Europe looks to be very much in play again, as Silvio Berlusconi has a shot at the Italian elections— which could blow up the current austerity-driven political consensus—and the economy of the eurozone as a whole continues to weaken, driven primarily by France.

February 20, 2013

In the last round of the Washington budget debates—the fiscal cliff—a compromise was finally reached, whereby the Bush administration tax cuts were extended for the vast majority of the population, while taxes went up on people with incomes over $400,000 (or $450,000 for joint filers). In addition, the expiration of the payroll tax waiver raised taxes on everyone with wage income.

You probably remember this. It was only a couple of weeks ago.

February 6, 2013

Yesterday, I posted an update on the rising risks in Europe. After I wrote that piece, I spent some time thinking about other risk areas that have fallen off the radar screen a bit and decided that today would be a good time to address those as well.

February 6, 2013

Off to a great start

January 30, 2013

So, gross domestic product—that is, the U.S. economy—declined a bit (by 0.1 percent, to be exact) for the fourth quarter of last year. Is this it? Is a recession starting? What about all the good news I’ve been discussing? Aaaaaaaaaaaah!!!

Okay, I feel better now. In fact, while no one wants to see a decline in GDP, if we have to have one, this is exactly how we want it to happen.

{kind=link}