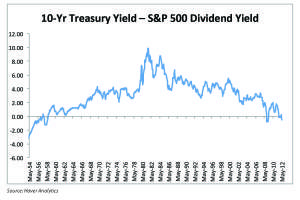

Back in the day, I understand, stock dividend yields were higher than bond returns. They had to be, you see, because stocks were so much riskier that investors demanded the return premium. Gentlemen preferred bonds.

June 29, 2012

Back in the day, I understand, stock dividend yields were higher than bond returns. They had to be, you see, because stocks were so much riskier that investors demanded the return premium. Gentlemen preferred bonds.

June 28, 2012

I have been looking for a metaphor that usefully and accurately describes the European crisis, and I think I finally have it. The moment of enlightenment came last night when I was talking with an advisor at Commonwealth’s Retirement Symposium (which looks to be fantastic for the second year running) about our kids. This advisor has teenagers, and as we were talking, I found my metaphor. I hasten to add that this is based on my experience—not that of the advisor and her kids.

When I was in college, through some colossal mistake, I was issued a credit card by Citibank, who must have held the theory that my parents would make good on my debt if (when) I overspent. To make a long story short, I learned an expensive lesson: my parents declined the opportunity to bail me out, default was not an option, and it required personal austerity on my part to pay off the credit card.

June 27, 2012

One of the changes I mentioned yesterday is that we no longer live in a world that is dominated by finance and economics. With most of my blogs over the last month largely dominated by financial and economic issues, that statement may seem strange. That’s because the discussion up to now has been backward-looking—it has dealt with problems that were created in the past and now have to be resolved. Looking forward, finance and economics will not become less important, as we will be dealing with those problems for a long time, but less dominant as a decision framework.

Another way to look at this situation is to consider it not as a decline of finance, but as a resurgence of other factors. One of these factors is the role of government. Since Reagan, the job of the government has largely been to get out of the way. Government is the problem, went the cry, and deregulation was considered an absolute good. Much good was indeed done, but, over time, I’ve increasingly been thinking that perhaps the old regulated world had its advantages as well.

June 26, 2012

I am a big fan of the Lord of the Rings movies. I would love to embed Cate Blanchett’s witchy Galadriel voice, saying at the start, “The world had changed,” because we are seeing this more and more in the news and in how we look at the world.

I put together a presentation a couple of months ago that talked first about the U.S. economy and then about how it fit into the world and what that meant for our future. As I developed it, I realized that there was actually a consistent narrative that went beyond the U.S. and economics. Simply stated, the primacy of economics and markets as an organizing principle was rapidly eroding and returning to a much more mixed environment of politics, geography (broadly defined), and economics. I will get into this some more tomorrow, including posting a copy of that presentation, but today I want to make a related but different point about how our perception of the world has changed—and how that will affect how we live going forward.

June 25, 2012

Short term, overall market activity is largely random. Unless, that is, there is some overwhelming new information that can, in fact, change the aggregate valuation level. We thought that might happen this morning, with the Supreme Court preparing to rule on Obamacare. As it turns out, we’ll have to wait three more days, until June 28, to find out whether a proposed restructuring of about 18 percent of the U.S. economy is constitutional or not.

To quote our vice president, this is a big #*%!-ing deal. I don’t want to get into the details of the policy: first of all, I’m not qualified, and second of all, I try to stick to facts rather than opinions here. The factual takeaway, though, is that the federal government has asserted a right to restructure nearly a fifth of the economy. Literally everyone’s life will be affected in one way or another.

June 22, 2012

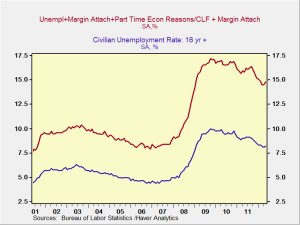

We talked yesterday about the unemployment statistics and about how what is generally reported is not so much misleading as it is incomplete. That discussion is actually—and not by accident—a good lead-in for today.

There has been a great deal of coverage of the slowing recovery and of how that slowdown might mean a recession. Let’s look at what this means both for now and into the next six months or so.

June 21, 2012

There is quite a bit of discussion in the press about the U.S. economy, much of which is misguided or misleading. One of the worst offenders is the discussion of unemployment, and I wanted to dig into some of the underlying data to discuss what I look at instead.

June 20, 2012

Two sets of meetings going on now are expected to help resolve the current financial and economic problems. The G20 meeting—followed by a meeting planned for this Friday of Germany, France, Spain, and Italy to prep for the eurozone summit next week—is one set, and the Federal Reserve meeting, which will end this afternoon, is the other.

The contrast between the two is instructive. On the one hand, the first set is a group meeting followed by a pre-meeting meeting for another meeting. The other is a regularly scheduled get-together with standard procedures and announcements. This basically describes the difference between European attempts to address problems and that of the U.S., and it illustrates why the U.S. response has been both more organized and more effective.

June 19, 2012

Yesterday, I shared my view that the European situation will probably be resolved, and the eurozone preserved, as the alternative could be a return to the conflicts that ripped the continent apart in the last century. The Greek elections were the latest crisis flash point, opening up the possibility of electing Syriza, a party that had pledged to reject the painfully negotiated bailout package.

June 18, 2012

I hope all you fathers out there had a great day. I had a wonderful time playing with my son, Jackson, who is 4 years old. We brought him home from Viet Nam about three and a half years ago, and he is a great kid.

June 15, 2012

There was more in the papers today about Europe, as the situation continues to evolve amid lots of hand-wringing about what can be done to save the region. The problem is not going away. We are facing a continuing series of what will be perceived as crises—a “hurricane season”—that will result from each country’s decision about whether to remain in the eurozone, and give up much or all of its budgetary and fiscal sovereignty, or go independent. Some, like Greece, might not end up with the luxury of being able to make the decision for themselves.

Right now, we are seeing Hurricane Spain, which will be followed shortly by others. The UK is putting flood walls in place—to extend the metaphor—and reports are that central banks around the world are readying rescue operations in case the Greek elections result in even more political and financial turmoil. What we have learned at this point is that volatility will certainly continue.

June 14, 2012

But not, perhaps, what you are thinking of. The economic shock I’m referring to happened a couple years ago at a conference given by Capital Economics, a consultancy we use. There, for the first time, I heard a very accomplished and respectable economist make a case for protectionism. I was stunned.

Not, he hastened to add, that protectionism was a good thing overall—it wasn’t—but he believed that the U.S. could potentially be better off with the imposition of some trade-limiting measures. Although we might have to pay for this benefit with larger losses elsewhere, the U.S. would be better off on a net basis.

June 13, 2012

The pain in Spain continues, with yields hitting a euro-area high of 6.8 percent—very close to what is widely viewed as the 7-percent red line that would compel a bailout. Intra-European political debates about how best to handle the situation are ongoing, with non-Germans demanding that Germany pay and Germany, understandably, looking for other options.

I don’t want to talk about that today, though, for a couple of reasons. First, because we already discussed it for the past two days and nothing material has changed. And second, because there is some U.S. economic news that warrants discussion.

June 12, 2012

As promised two days ago, today we have more on Europe and China. The Spain situation continues to evolve, and the markets gave a resounding vote of no confidence on the bank rescue. After first rallying, equity markets either ended flat or down. Spain’s 10-year bond yields climbed to almost 6.5 percent and Italy’s to more than 6 percent.

The fallout went beyond the financial markets. Cyprus became the fifth European nation to seek a bailout, and China stepped up its stimulus by encouraging banks to lend more. The president of the European Commission called for all 27 countries to submit to common banking supervision and regulation. The front page of New York Times included an article titled “Worry for Italy Quickly Replaces Relief for Spain.”

June 11, 2012

The headlines this morning are all about the Spanish banking system rescue, with front-page, top-of-the-fold articles in the Financial Times, the Wall Street Journal, and the New York Times.

June 10, 2012

This is the inaugural post in Commonwealth’s new blog, The Independent Market Observer. It is being written on my birthday, which makes it somehow nice that we’re kicking off this blog on the same day I came into the world.

For those who don’t know me, my name is Brad McMillan. I am Commonwealth’s chief investment officer and will be the primary author of the posts here. I will also bring in content from other members of the Commonwealth team where it makes sense—we have a wealth of talent here, and I want to share that—but I see this as my soapbox from which to highlight, on a regular basis, what I think is important in the economy and markets.

June 6, 2012

Sell in May and go away?