I had an interesting talk with a reporter for a major newspaper yesterday about the debt ceiling issue. She wanted to know what we were doing about it and what changes if any we were making to our allocations.

August 30, 2013

I had an interesting talk with a reporter for a major newspaper yesterday about the debt ceiling issue. She wanted to know what we were doing about it and what changes if any we were making to our allocations.

August 29, 2013

One of my earliest musical memories is listening to the song “The Sound of Silence” by Simon & Garfunkel playing on a reel-to-reel tape recorder that my father had brought home when I was very young. I am sure that I had heard music before— on the radio at a minimum—but I remember being very struck by the beauty of the song, particularly the harmony of the voices, in a way that I had never been before. I actually trace my interest in music to that particular song and that particular moment.

I was remembering this in the context of a quiet week in Maine, where I have had the chance to do quite a bit of hiking in fairly unfrequented areas. The area around my cottage has also been quite empty during the week, so I have had a chance to listen to considerably more silence than is normally the case. Silence very definitely has a sound of its own, and, as much as I love Jackson, quiet he is not.

August 28, 2013

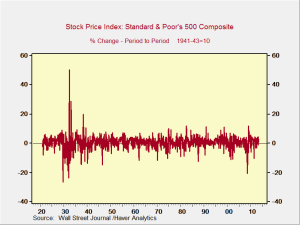

With the S&P 500 down almost 5 percent from its peak, and a drop yesterday, I am starting to hear from investors who are asking, “What is going on? Do I need to worry?” The short answer is, it depends on your portfolio and your time frame.

I have written extensively about how the market is either somewhat or very richly valued, based on historical standards, and how most of the appreciation this year has come from investors paying more for a given stream of earnings, rather than from an increase in the earnings themselves.

August 27, 2013

In what I really hope is an apocryphal story, it is said that frogs don’t notice small temperature changes. You can, therefore, put a frog in a pan filled with cold water, and, as long as you heat it very slowly, you can actually boil the frog without it jumping out. If you keep the temperature changes slow enough, it will never realize that the heat is rising to harmful, and then fatal, levels.

I have, obviously, never tried this, but something similar has been happening in the U.S. economy. I am pleased to find, however, that people appear to be somewhat smarter than frogs. The heat I’m referring to is the pending debt ceiling crisis.

August 26, 2013

I haven’t written much about education recently, but now that school is starting back up, it’s time to take another look. My oldest nephew, Jake, is entering college this week here in Boston, which adds a certain amount of immediacy to the discussion.

When I compare the experience Jake will have with what my five-year-old son, Jackson, might have years from now, I expect there will be significant differences. First, Jake will be starting at an established university, with a physical campus, and take most or all of his classes sitting in a lecture hall—just as his parents and I did. For Jackson, I doubt very much that will be the case.

August 23, 2013

I will be taking some time off next week. I will still be blogging every morning, but I plan to spend the rest of each day doing some resting and recreating. There are a number of issues I want to think more deeply about before reengaging, and this will give me a chance to do some long-deferred reading and thinking.

August 22, 2013

I had the chance yesterday to be a guest on the Bloomberg Radio program Taking Stock, which was an awful lot of fun. The hosts, Pimm Fox and Carol Massar, are both smart and well informed, and the other guest, Kevin Divney, had some very interesting views and was a pleasure to bounce ideas off of.

August 21, 2013

Over the past week or so, I’ve had the chance to sit down with several groups to discuss how the economy and the financial markets are evolving. Each time, I’ve laid out many of the arguments, along with supporting data, that I’ve made here on the blog. Briefly, the real economy is improving, and growth can reasonably be expected to accelerate for the rest of the year; interest rates are going to remain volatile and increase over time, although they may drop back a bit in the short term; and stock markets are overvalued and risky.

But what if I’m wrong?

August 20, 2013

I’m meeting with the investment committee of one of our advisor groups this morning, and, in preparation, they sent me a list of very good questions they want to discuss. We’re also planning to start an “Ask Brad” section of the blog to address common questions. With both of these pending, and a couple of questions on everyone’s mind right now, I thought I’d start out with the big one, which is, of course, What are interest rates going to do?

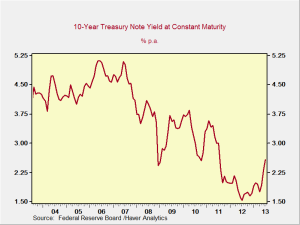

Interest rates have moved higher again over the past week. What is driving the current spike in rates, as I’ve written before, is price discovery. As the Fed moves closer and closer to tapering away its bond buying, the market will increasingly be driven by supply and demand factors. In recent weeks, foreigners have been selling bonds, as have domestic banks. When and if the Fed starts to taper, demand will decrease even as supply is likely to continue to increase from the increased selling. When demand goes down and supply goes up, prices drop. In the case of bonds, this means yields go up.

August 19, 2013

August has been tough for the stock market. We’re now down a bit over 3 percent, even as interest rates continue to tick up. Based on the last time tapering hit the markets, we may have more downside risk ahead.

August 16, 2013

As more or less promised yesterday, let’s talk about the market. Yesterday, we saw two interrelated events: interest rates ticked up again, and the stock market declined. Why? Will it continue?

First, we’ll look at the rise in interest rates. I use rates on the 10-year Treasury bond as a proxy for rates as a whole, as many other financial instruments use the 10-year Treasury as a basis off which to price. This is common in the market.

August 15, 2013

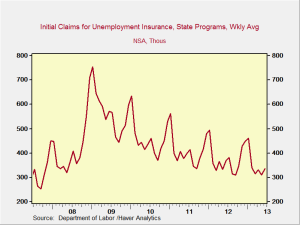

Looking for new news today is hard. There are a lot of good economic stories—Europe’s economy has started to grow again, initial unemployment claims have come in at a six-year low, consumer borrowing has picked up again, among other stuff—but I’ve written about that several times over the past couple of weeks.

I could talk about the drop in the stock markets this morning or the uptick in interest rates, but I’ve also covered those topics multiple times lately, most recently yesterday. No doubt I’ll return to them again in the next couple of weeks—maybe even tomorrow, depending on how the market closes today.

August 14, 2013

Several advisors have called me over the past couple of days, asking about various doomsayers predicting various forms of calamity. A dollar collapse is one popular theme; another is a collapse of the stock market, of “up to” 90 percent, according to one reported expert.

Make no mistake: I’m concerned about stock market valuations, as I have written extensively. It’s entirely possible we will see a correction, quite possibly a significant one. In fact, at some point, a significant correction isn’t just inevitable, it’s normal and even healthy. Let’s look at history.

Several pieces of good economic news have come in that are worth highlighting. The most important is U.S. retail sales, which is up 0.2 percent. That might not seem like anything to cheer about, but this is a case where it’s important to look at the underlying figures rather than just the headline.

The overall figure was dragged down by drops in auto sales and building material sales. While not positive, both of those figures are still at very high levels, and, even with the slight decline, growth rates remain at levels consistent with faster growth overall. Gasoline sales increased, which was a positive factor, but this is counterintuitive, as it depends to some degree on higher gas prices, which are actually harmful to the economy as a whole. These three series are also volatile, to the extent that there is a separate statistical series that excludes them in order to provide a better indicator of underlying consumer demand.

August 12, 2013

One interesting trend recently has been the outperformance of the U.S. and other developed markets over emerging markets. A number of factors are behind this, notably capital flows, but shifting relative growth rates have been a primary driver. In this post, I want to take a look at the basic sources of growth to see how this trend might evolve over the next couple of years.

August 12, 2013

— Guest post from Peter Essele, senior investment research analyst

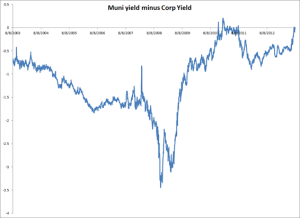

After the large uptick in rates and subsequent outflows from fixed income funds, the waters seem to have calmed recently, and investors are now beginning to move back into the space. One area, however, has continued to see outflows. While the taxable side of things only witnessed 4 weeks of outflows before a return to positive flows, the municipal bond category has recorded 13 straight weeks of outflows. Why is this happening?

August 9, 2013

It’s a slow news day on the economic front, and Jackson and I are on a plane to visit his grandparents, so I thought I’d extend the conversation about personal quantification and investing.

The idea “if you can’t measure it, you can’t manage it” is just as applicable in personal goals as it is in business. Maybe more so, because in your personal life you don’t have a net profit line to tell you whether you’re doing well. I’ve found that measurement can provide the impetus to keep going and to modify behaviors to be more effective.

August 8, 2013

Over the past couple of years, I’ve made a concerted effort to be healthier, exercise more, and weigh less. This was prompted by a lot of huffing and puffing from carrying Jackson around, as well as the realization that, the way I was, I would be the “fat dad,” which I was very unwilling to accept.

I had a lot of success, losing about 50 pounds peak to trough. Unfortunately, I then put about 25 of it back on and am now working on getting rid of that again. Being a research geek, I found myself looking at a great number of websites and books, which, in many cases, prescribed opposite courses of action. The diet industry has literally tens of thousands of books and, it seems, even more websites. Many of the diets, if you look into them, are actually repackaged and sold under new names every decade or two.

What seems conspicuously absent in many of these plans, though, is clinical data on what works. What’s almost entirely absent is an analysis of which plans work for different types of people. Even for plans with supporting clinical data, there is a presumption that one size fits all. I doubt that’s the case, since it never has been in any other situation. I suspect that many or all of these plans work for some people, if they stick to it, but not for others.

The other real problem in evaluating the success of any weight loss plan is the selection bias in most of the available data. People who fail on a diet rarely write about it and are certainly never included in the advertising.

For anyone who cares, I seem to have found a mix that works for me, which consists of the following:

I don’t suggest this will work for anyone else, but for me the results are substantial—and, more important, sustainable. This is what killed me before when I put a lot of the weight back on: what I was doing then wasn’t sustainable.

For many people, investing falls under the same category—should do, don’t want to do—as weight loss. It’s something that will pay future benefits but cause present pain. For those people, I think weight loss lessons have some value.

First, set up a regular habit that’s easy to keep. I like omelettes, for example, and the cafeteria in the building next door does a great one—very easy. For my retirement investing, I set a deferral percentage that comes directly out of my pay. If I can save more, I set up a similar direct deposit to an investment account. Another example might be a credit card that automatically deposits some percentage of purchases to an investment account.

Second, use a preset method to determine allocations and rebalance. For many people, a financial advisor is an ideal solution, but other web-based programs are also becoming available. I regularly review and rebalance my portfolios using a predetermined decision rule, so I don’t have to think about it, just execute. This makes it much easier to actually do. Walking while reading is a good example of this—I just grab my reading material and head to the treadmill. No thinking, just do it.

Third, review the analysis behind your decision rules on a regular basis. As with dieting, there are tons of investing options, many of which really work—but you have to be able to stick to them. If your process isn’t working for you, you need to recognize and change that. I have reviewed much of the research and concluded that what I’m doing will work for me, and I’m monitoring the results to make sure it is.

So far, so good.

August 7, 2013

I wrote last Friday about the return to political economy, and one of the points I raised there was the breakdown of the consensus on the right form of government, the economy, and the relationship between them.

August 7, 2013

I am pleased to say that I’ve been asked to write another post for the CFA Institute’s Inside Investing blog. The idea for this one was to consider what we believe but can’t prove in investing. I like these posts because they move away from the day-to-day concerns about what to buy or sell and into the underlying assumptions that help determine the decisions we make.

Hope you enjoy reading it nearly as much as I did writing it.

August 6, 2013

One of the problems with what I do is keeping everything current. The gap between when I prepare a presentation and when I give it can sometimes lead to awkward results.

August 5, 2013

I’ve been doing a lot of thinking about alternative investments over the past couple of weeks, from a number of different perspectives. But before I proceed any further, I want to make clear that the content of this article does not constitute a recommendation to buy or sell any investment of any type.

Last week, I spoke with an institutional private equity manager, a hedge fund manager, and a major Wall Street financial institution about how they can better access retail investors to sell alternative products. This kind of interest isn’t particularly new; what is new is the recognition that retail investors can be the preferred capital source instead of an afterthought. As more and more companies start to realize this, we can expect to see the current group of offerings double and triple in size, with new players moving into the market and providing strategies and products that simply aren’t available right now.

August 2, 2013

One of my major themes last year was the return of political economy. This is the discipline that Smith and Ricardo, among others, invented, and it was called that because they understood very clearly the relationship between politics and what we now call economics. The notion of considering them independently would have seemed nonsensical.

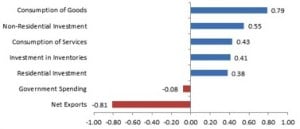

After I wrote yesterday’s post, I was discussing the results with a colleague who was much more downbeat than I had been. “Only 1.7 percent!” he pointed out, maintaining that this is quite a low growth rate, well below those in previous recoveries, and nothing to get excited about.

You know what? In absolute terms, he’s right. The 1.7-percent growth rate is disappointing based on history, is not a level that will make us all rich, and certainly needs to increase. But to me, that’s not the point.

{kind=link}