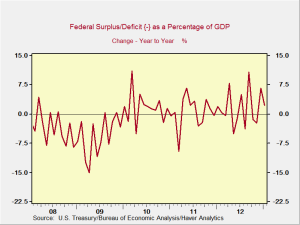

The deficit has dropped off the radar for a bit, what with the agreement to postpone debate about the debt ceiling and the generally improving economy, but recent events make it a good idea to check in and see where we are.

April 30, 2013

The deficit has dropped off the radar for a bit, what with the agreement to postpone debate about the debt ceiling and the generally improving economy, but recent events make it a good idea to check in and see where we are.

April 29, 2013

Over the past year, I’ve written about a number of issues that touch on demography, explicitly invoking it in discussions of employment and future growth. Like the group of blind men examining the elephant, however, I haven’t really considered the thing as a whole.

Demography, the study of the structure and characteristics of human populations, is almost unique in the economic universe in being something we can forecast with a great degree of certainty. We know, for example, how many people were born in 1965—that won’t change once the year is over—and we have a very good estimate of how many have died or had children since then. Unlike, say, employment, demography evolves over decades in a predictable way.

April 26, 2013

We’ve been talking about how the U.S. real economy, despite a second-quarter slowdown, continues to grow. The Fed by and large agrees, with several governors weighing in over the past couple of weeks to say that they see a sustainable recovery in place and that it’s time to start thinking about when and how to begin pulling back. You might be forgiven for thinking “Hooray!” After all, isn’t sustainable growth what we’ve been working toward for the past five years?

Although we do seem to have sustainable growth from multiple sources—housing, autos, and energy, among others—much of that growth is driven by current low interest rates, especially in housing. When the Fed starts pulling back, there is a reasonable possibility of higher interest rates, which will at least slow that growth.

April 25, 2013

Several data points have come through in the past couple of days that support some thoughts I’ve had for a while. I think it’s constructive to take a look at them to determine how we can expect the economy and financial markets to evolve in the near future.

April 24, 2013

Is it possible to predict the stock market? As usual, it depends on what you mean. If you mean determining where the market will close today or tomorrow, or what a particular stock will do next week, the answer is no. It’s when you get into longer time frames, or larger portfolios, that things get interesting.

It also depends on what you mean by “predicting.” Are you, for example, looking at calling an exact number or just seeking an idea of likely outcomes? If the former, you’re out of luck; if the latter, you can probably make some headway.

April 23, 2013

Yesterday, we talked about how the opportunity cost of not spending on defense might in the end be greater than the spending. Today, I’d like to do the same for social security.

I don’t believe the case for spending is clear here, and I’m mindful of the weakness in the opportunity cost argument. After all, if I bought all of the great deals I get in my e-mail every day, I would be bankrupted by the savings. But that’s a different post.

April 22, 2013

I was in Virginia late last week, speaking to a group of clients, and had a couple of interesting conversations that are worth expanding on here. To start off, we talked about what the U.S. is actually spending its money on, and how and whether it made sense to cut. This is a slightly different take on the spending discussion than you normally see. Typically, the discussion is based on the assumption that spending is more or less set; the issue is how to cut, rather than whether cuts make sense.

April 19, 2013

I am in Virginia today and tomorrow, speaking to groups of clients. With no major economic stories going on, I thought I would do a couple of quick hits on various topics.

April 18, 2013

As I wrote after Cyprus, I moved from a not-at-all-certain belief that the euro would make it, for political reasons, to a just-as-uncertain suspicion that it would not (also for political reasons). Recent events continue to widen the gap between the “make it” and “not make it” conclusions.

When Greece first defaulted, the narrative was all about irresponsible Greek borrowing, with the clear implication that they had it coming. News coverage focused on early retirement, state pensions at 50, and low tax compliance. In fact, when default hit, imports of necessary goods such as medicines also essentially stopped for most of the population. Very little of that made it into mainstream coverage.

April 17, 2013

On the heels of yesterday’s post on risk, outliers, and uncertainty, I saw an interesting article today in the New York Times. It discusses a recent paper highlighting potential errors in the work of Carmen Reinhart and Kenneth Rogoff, authors of the influential 2010 economic study “Growth in a Time of Debt” and the book This Time Is Different.

Covering financial crises in many countries over the past several centuries, Reinhart and Rogoff’s (RR) massive study draws the conclusion—controversial in certain circles—that, when a country’s overall debt exceeds a certain level with respect to the size of the country’s economy, expressed as GDP, future growth declines. It is used as an argument against excessive government spending and debt, particularly here in the U.S.

April 16, 2013

Like everyone else, I have been affected by the terror attacks of the past couple of decades. I mourned those killed in 9/11, cried for the Sandy Hook children, and sat appalled at Oklahoma City, but the Boston attacks have hit home the hardest, literally. I have never been to Oklahoma City, never lived in New York, so as much as it hurt, it was abstract—removed.

Not this time. My wife and son easily could have been at the finish line for the Boston Marathon. They were at home, working in the back yard, but they could have been there. I have friends who work in that area and had gone down to see the race. I haven’t heard that any of them were injured, but it could have happened.

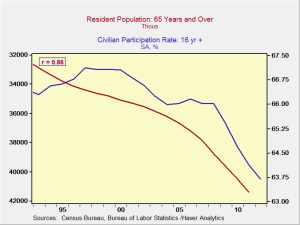

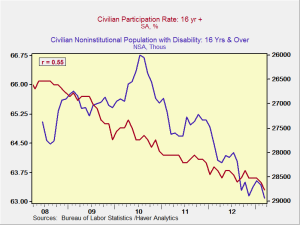

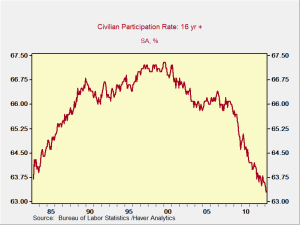

Several times over the past couple of months, I’ve mentioned that, while we certainly have an unemployment problem now, changing demographics will mean that the U.S., along with most of the developed countries (and China!), will eventually have a labor shortage. Hard to believe, I know, but then again, in 2005, most people didn’t believe that the housing market could ever go down.

I’ve also noted many times that part of the declining unemployment rate may be due to older workers retiring (to put it at its most favorable) or simply giving up on the labor market. As workers get older, a trend that is continuing, eventually they’ll simply drop out of the labor force in one way or another.

April 12, 2013

The economic stats just keep bouncing around. Although no single statistic is worth getting too excited over, the general trend of the data is pretty indicative, and what we are seeing is a decline in growth after the strong first quarter.

April 11, 2013

We will be hearing quite a bit about the Chained Consumer Price Index (chained CPI) over the next couple days, though most of the details don’t matter. It’s the first of two major takeaways from the president’s proposed budget.

For the sake of completeness, here’s the definition of chained CPI. What matters for the average citizen, however, is one thing: chained CPI increases more slowly than the inflation measures that are currently used, the CPI-U (the CPI for All Urban Workers) and CPI-W (the CPI for All Urban Wage Earners and Clerical Workers). By shifting the measure used, payments for social security will increase more slowly over time.

April 10, 2013

I love alliteration. A game my family plays on long car trips is to see how many words starting with the same letter we can string together and still make sense. I hold the record so far with something like Cape Cod Canal Commission Community College Cheerleading Co-Captain’s Conference Center classroom chatter, or CCCCCCCCCCCcc. Top that!

The topic for today, however, is the budget battle. We now have three budgets out there—the Senate Democrats’, the House Republicans’, and the President’s. While none of them will be passed as presented, we can reasonably define the box that the final budget will fit in. I plan to do a detailed analysis and comparison in the next couple of days.

April 9, 2013

“Margaret Thatcher RIP,” I tweeted yesterday, but in retrospect, that’s probably the least likely outcome. Wherever she ends up, peace is the last thing I would expect. If heaven, she’ll be offering God suggestions for how to run the world better; if hell, she’ll be planning a revolt. Love her or hate her, there’s no doubt that Margaret Thatcher changed Britain and, to a much lesser extent, the world.

I say “to a much lesser extent” because, as the current European situation plays out, it is becoming increasingly apparent that we’re reaching a Thatcherite breakpoint. To paraphrase one of my favorite quotes of hers, the problem with socialism is that eventually you run out of other people’s money. Europe, especially the periphery, is now at that point.

April 8, 2013

Unsurprisingly, last week’s disappointing employment results have generated quite a bit of discussion. The most interesting part for me has been a quantitative finding from Ned Davis Research: if you compute the actual hours worked, given the number of jobs and the increase in the average work week, it’s the equivalent of another 328,000 jobs added. Therefore, the aggregate hours worked—the actual labor input into the economy—actually rose 0.3 percent rather than declining, and the increase is pretty strong, above the 12-month average.

April 5, 2013

As I mentioned the other day, the past couple of years have seen a slowdown from a strong first quarter to a weaker second quarter, and it seems like this year will be no exception.

This morning’s employment reports were a serious disappointment. Job growth dropped across the board, with an increase of 88,000 in nonfarm payrolls—down from 268,000 in February and less than half the expected 190,000. Although the decline was partially offset by upward revisions in the previous months, there’s no denying this is a significant letdown. Adding to the bad news was a slowing in wage growth, from 2.1 percent to 1.8 percent on an annual basis, with wages staying flat month to month.

April 4, 2013

In my response to David Stockman’s op-ed piece in the New York Times, I stated that our problems are, in fact, solvable, and that we are—however slowly and painfully—in the process of solving them.

Not everyone is convinced, to put it mildly, and to state it is not to demonstrate it. Looking through today’s papers, though, I found a couple examples of exactly what I was talking about.

April 3, 2013

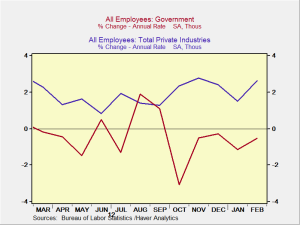

For the past couple of years, we’ve seen a strong first quarter followed by a much weaker second quarter. Initial signs suggest that the pattern may continue this year as well. Should we expect that—and, if so, what would it mean?

First, the good news: the first quarter was very strong. Economists are estimating that growth could have been as strong as 3 percent, which is well above expectations. Private employment continued to grow, with signs of an increasing growth rate over the past year, while government employment recovered somewhat after a tough fourth quarter, as shown in the chart below.

Several people have forwarded me “State-Wrecked: The Corruption of Capitalism in America”—a recent New York Times op-ed by David Stockman, former budget director for President Reagan—and asked for my thoughts. Having read through the piece, it’s actually not that easy to respond, as Mr. Stockman seems to be all over the place. In fact, I’m not sure exactly what he’s saying other than that we’re all doomed.

Trying to pick out the different parts of his argument, I come up with following. First, abandoning the gold standard was a huge mistake and has led to fiscal and moral debasement. Second, the Fed has been the agent of said debasement, printing money to enable the federal government’s wanton spending. Third, Wall Street has captured both the Fed and Washington, D.C., and is using them to enrich itself. Fourth, the 2008 financial crisis would have burned itself out and we would have been fine had the government not intervened. Fifth, our fiscal situation is not only worse than admitted but beyond hope. We cannot solve our present problems and face a future of poverty. In short, under the present system, we’re doomed, and we largely deserve it for past sins. Thus endeth the lesson.

At the end of the quarter, we all look at our statements and evaluate how we’re doing. Depending on the results, we either congratulate ourselves or start to ask what went wrong—and what we can do about it. The implicit assumption here is that we are in control of our investments.

To a great extent that’s true, of course, but the markets are beyond anyone’s control. Trying to manage that uncertainty has been the great quest of modern finance. The management of uncertainty is also characteristic of another financial endeavor: gambling.