The real news from yesterday is, of course, that the Boston Red Sox won the World Series at Fenway for the first time since 1918. Nothing else even comes close. End of post.

October 31, 2013

The real news from yesterday is, of course, that the Boston Red Sox won the World Series at Fenway for the first time since 1918. Nothing else even comes close. End of post.

October 30, 2013

I’ve written before about the potential problems lurking in the financial system. LIBOR, for example, was something I started covering last year. Looking at the papers today, though, even I am surprised by the sheer number—not to mention magnitude—of the problems that are showing up.

In just one of today’s papers, the Wall Street Journal, we have the following articles:

October 28, 2013

One of the stories in today’s Wall Street Journal describes how a number of U.S. cities are coming to terms with their inability to pay their obligations. Earlier articles in the WSJ and elsewhere gave some details—specifically, in years when investments did better than expected, many cities took the excess returns to add to payments, making the cookie jar smaller when the inevitable underperforming years came. They had confused the short term with the long term.

I get the same kind of question, in a different form, when I speak with investors. Should we invest in the stock market? Well, I say, what is your time frame? Over the long term, you absolutely have to invest in the market. Over the short term, you might be best off not doing so. Is this a one-time investment or a continuing stream of investments? How old are you? And so on.

October 25, 2013

This morning, I had the chance to talk with the lead fixed income (bond) portfolio manager from one of the largest Chinese mutual fund companies. Arranging the call was a bit difficult, what with the difference in time zones and our travel schedules (which is probably a metaphor for something or other), but the conversation turned out to be well worth the effort. As an aside, we really do live in a miraculous age, where you can talk to someone on the other side of the planet.

October 24, 2013

While rushing between planes yesterday, I had a good conversation with one of our advisors, who was preparing a talk for his clients about whether the recovery is real. Specifically, he was concerned about the fact that money velocity is so low.

October 23, 2013

I’m at the airport waiting to board a plane, so this will be a short post. Fortunately, today it writes itself. I mentioned last year how proud all of us here at Commonwealth’s research and asset management groups were to be named, again, to Financial Advisor and Private Wealth magazines’ list of investment research and wealth management all-stars. Last year, we had more winners than any other firm, for the second year in a row.

Well, we’ve done it again, and you can read the article here. Once again, we have the greatest number—and scope—of winners, and we’re the only major broker/dealer included.

October 22, 2013

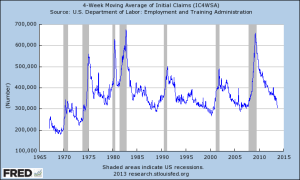

Part of the problem with the government shutdown was that many of the economic reports we rely on were collateral damage. In the absence of data, everyone (including the Federal Reserve) has been flying blind. With the government back at work, the catch-up process has begun, and the September employment data was released this morning, giving us our first look at the effects of the (then looming) shutdown. A number of private data points have also been released since then, so I think it’s now possible to start to consider the economic damage.

The news on employment is not good. Total nonfarm payrolls were up by 148,000—much less than the expected 180,000 and well below the previous month’s figure of 193,000, which was adjusted up from 169,000. On the face of it, employment growth took a real hit here. While we can’t make too much of one month, the magnitude of the decline, combined with the fact that it took place before the shutdown, suggests that the actual shutdown damage will be worse. Both the unemployment rate and underemployment rate did drop slightly, from 7.3 percent to 7.2 percent and 13.7 percent to 13.6 percent, respectively, but even that news isn’t particularly positive, as the drops weren’t driven by job gains but by changes in the workforce.

October 21, 2013

Now that we are entering peak week for earnings reporting, it is time to take a look at what that means for the stock market. We have some data so far, but not much, so I want to defer a detailed analysis to next week. For the moment, let’s look at financials.

I wrote back on June 11 and July 10 about the pressure the financial services industry, particularly banks, was likely to come under and the negative effect that was likely to have. Specific points I made were regulations, capital requirements, more operational scrutiny, slowing mortgage demand, and others.

October 18, 2013

In the past 24 hours, I’ve had several discussions that centered on the question “What do we do now?” During one, on Fox Business News yesterday afternoon, the anchor pointed out that, even as I was cautious on equities, the market had climbed a wall of worry all year—and looked likely to continue to do so. Does that make caution on equities wrong? Similarly, I was talking with a Wall Street Journal reporter this morning about where the market was going, and we got into the continuing government confrontation, earnings, and the real economy—all without coming to any real conclusions.

First things first: The fact that the market keeps going up doesn’t mean everything is all right. Under that standard, the housing market was perfectly fine in 2007, so I don’t think the fact that the market is rising means caution is inappropriate.

October 17, 2013

“Pro football is like nuclear warfare. There are no winners, only survivors.” — Frank Gifford

That pretty much sums up my take on the most recent confrontation in Washington, DC. No one won, and everyone lost. The Republicans took a huge poll and public relations hit, for no gain at all. The Democrats didn’t lose as much but, in many ways, came out looking just as petty and political. Congress has hit all-time lows in public support, something I would have said was almost impossible, and the White House has been roundly and justly lambasted for its lack of leadership.

Recently, I was invited by the CFA Institute to contribute some thoughts to a discussion about why the Fed doesn’t forgive the debt. My commentary was published, and I’ve received some very nice feedback on it. You can read it here.

October 16, 2013

I’ve spent quite a bit of time over the past couple of days talking with advisors about the potential consequences if the government doesn’t make a deal in time. Yesterday, I did an interview with Chuck Jaffe of MoneyLife Radio that focused on exactly that. As we move closer to the supposed drop-dead date—that would be tomorrow—I thought it would be useful to look at how I’m thinking about investing.

First of all, let’s hit a couple of points I’ve made before. In the longer term, the events of the next week or so will not be significant. The U.S. economy is diverse, solid, and set to outperform for at least the next 20 years and probably more. Markets will reflect that growth, and, longer term, you absolutely want to be invested here. At the same time, current valuations are at the very least not cheap, and it’s been some time since we’ve had a correction in the U.S. stock market. Quite apart from the current situation, we are overdue. Again, this isn’t to minimize what might happen, simply to put it in context.

October 15, 2013

First of all, thank you to everyone who wrote nice things about my appearance on CNBC yesterday—much appreciated. It’s fun to do that kind of appearance because you never know exactly what will be discussed, and you have to prepare. Keeps me on my toes!

This will be a short post because I’m in New York attending a conference on ETFs put on by iShares. ETFs, for those who haven’t run into them, are exchange-traded funds—that is, a portfolio of assets (stocks, bonds, what have you) that is traded like a single share of stock. They are similar to a mutual fund that tracks a specific stock or bond index, such as the Barclays Capital 1-3 Year Treasury Index. ETFs trade on one of the major stock markets and can be bought and sold throughout the trading day, like a stock, at the current market price. And, like stock investing, ETF investing involves principal risk—the chance that you won’t get all the money back that you originally invested—market risk, underlying securities risk, and secondary market price. ETFs have become a major part of the investing landscape over the past several years, changing the way many people and institutions invest.

October 14, 2013

Over the weekend, I traded e-mails with one of our advisors, who pointed out that I hadn’t yet done a complete explanation of the situation in Washington, DC. Sure, I’d touched on various aspects of it, but I hadn’t really looked at the thing as a whole. So here’s my take. Thanks, Alex, for the great idea!

The Big Picture

October 11, 2013

One of the great things about working at Commonwealth is the depth of knowledge of our team. Today, we have another post from Peter Essele, one of our portfolio managers and analysts.

October 10, 2013

The consequences of the debt ceiling standoff and government shutdown continue to reverberate. Markets are increasingly showing signs of nervousness, with excess volatility tracking news reports as they come out of DC.

I’ve been reviewing my posts and articles from the last time we went down the debt ceiling crisis road, and marveling a bit. Trillion-dollar coin indeed! That post proved to be prescient in a lot of ways, although 10 months early. The options I outlined there remain the most probable this time around, but no one has been trotting them out so far. Instead, the discussion has revolved around how to make payments once we run out of money.

I don’t like the spirit of despair that this kind of planning reflects, and I think I have a better idea about how to solve the problem. It requires no issuance of coins, no scrip rather than cash—although the difference is small—and no constitutional confrontation.

October 8, 2013

As we move into the second week of the shutdown—and another day closer to running out of room to maneuver around the debt ceiling—cracks are starting to appear.

On the political level, there’s an apparent disconnect between a White House potentially willing to accept a short-term rise in the debt ceiling and a Senate holding out for a longer-term deal on the Democrat side. In the Virginia governor’s race, the Democrat appears to be gaining an edge from the shutdown. The Senate Democrats are talking about passing a clean continuing resolution themselves, rather than waiting for one from the House Republicans—who have been taunting them about their unwillingness to force Democrat senators to make a potentially tough vote. In short, we’re seeing the usual political circus.

October 7, 2013

The government shutdown has gotten most of the press coverage so far, but there is a related and bigger issue pending in the next couple of weeks: the debt ceiling. Although the federal government has partially shut down, it continues to spend money on many items. Normal government financing requires regular additional borrowing, as we typically spend more than we take in.

October 7, 2013

I hate writing about politics, I really do. But, as we’ve seen repeatedly over the past couple of years, politics is now economics, and, therefore, it behooves us to get to grips with what that means for our country—and our investments.

One of the driving memes about Obamacare has been that it socializes a large section of the economy. The Republicans use this as an argument against, while the Democrats by and large see it as a feature, not a bug. The destination on the horizon, for both, is a more European polity. That means slower growth and stagnation for the Republicans and more social justice for the Democrats—in any event, a more European-style economy.

The market has bounced around without a lot of direction over the past couple of days, popping up this morning after a rough showing yesterday. What’s going on?

Ultimately, stock prices reflect corporate earnings per share, and the bouncing prices can credibly be tied to expectations about what the government shutdown and potential debt ceiling confrontation will mean for those earnings. The changes in prices reflect the market’s attempt to come to grips with what we can expect to see over the next couple of quarters.

October 4, 2013

Despite turbulence, a strong September and third quarter

Despite economic and political turmoil, markets performed well across the board in September, with almost all asset classes showing strong returns, reversing many of August’s losses. This also resulted in positive overall quarterly performance.

Since there’s really no movement in the DC stalemate, I thought I’d highlight some good news today. I continue to keep an eye on the government, and the risk grows daily. At the same time, though, it’s important to remember that there is life beyond the Beltway (for those who don’t know, that’s the highway surrounding Washington, DC) and that the real economy is actually doing pretty well. Even as DC stares and Wall Street trembles, Main Street has some news to be glad about.

1. Initial jobless claims remain quite low, at 308,000.

October 2, 2013

With the government shutdown entering its second day—and apparently no negotiations under way between the Republicans and Democrats—the prospect of an early compromise agreement doesn’t look good. A headline in today’s Wall Street Journal, “Capital Digs In for Long Haul,” pretty much says it all.

The markets yesterday seemed to shrug off the shutdown. Much of the commentary has been along the lines that the shutdown is no big deal, a compromise will certainly be reached, and this is actually a buying opportunity. That may end up being the case, but I think it makes sense to at least consider the other possibility: that the stalemate continues until the Treasury runs out of accounting tricks to avoid the fact that the government is now at the debt ceiling, which should be in the next couple of weeks.

October 1, 2013

For the first time since 1995–1996, the U.S. government has been shut down in a dispute over the federal budget. Now that it has happened, we can start to assess the damage, as well as evaluate how the dispute is likely to play out.

Before we do, there are a couple of important things to keep in mind. First, we made it through the 1995–1996 shutdown, and we will make it through this one. Second, although there will be damage, it will be limited. Just as with the sequester spending cuts, the damage will be absorbed and the economy will return to growth. This too will pass.

“In spite of the cost of living, it’s still popular.” — Laurence J. Peter