I hope everyone enjoyed the long weekend as much as I did. My son, Jackson, and I built a small working wooden catapult and a fire-dog house using his cardboard blocks. And he went skating and to a SteveSongs concert with his mom.

January 22, 2013

I hope everyone enjoyed the long weekend as much as I did. My son, Jackson, and I built a small working wooden catapult and a fire-dog house using his cardboard blocks. And he went skating and to a SteveSongs concert with his mom.

January 18, 2013

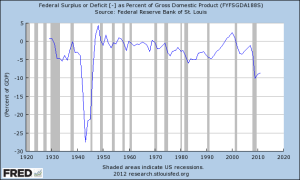

A popular talking point these days is that the deficit over the past several years has been the worst since World War II. That’s absolutely true, as you can see from the chart below, but the statement misses a key point.

January 15, 2013

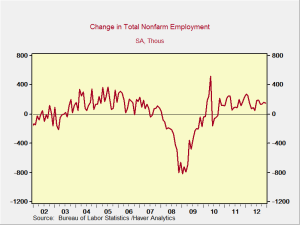

Following on the review of how well the housing market is doing, I thought I would take a look at employment.

January 14, 2013

One of the wonderful things about the digital age is the emergence of mash-ups, where people combine elements of existing art in new ways. The idea has been around for decades, of course, but the Internet and digital technology have made it even easier to create and distribute.

January 10, 2013

In part 1 of this post, I talked about what inflation is and how a moderate level has actually been good for the economy over the past couple of decades. That changed in 2008. Asset prices, particularly in housing, had inflated to an unsustainable level. The inflation measure the Federal Reserve (Fed) had been watching was based more on consumer consumption prices and less on asset prices. The asset price inflation got out of control and eventually collapsed. Because much of the financial system at that time was exposed to those asset prices, a financial crisis ensued.

January 10, 2013

I’ve said it before and will say it again: the debt ceiling debate, coming shortly, is the real thing we need to worry about. The deal over the fiscal cliff settled the immediate risk to the economy—although everyone’s taxes went up, they went up much less than they could have, and spending power was therefore preserved. Spending cuts, which will hit at the same time as the debt ceiling, will also be a headwind to the economy, but they are necessary and can be phased in to cause minimal harm. The one thing that could really blow us up is failure to resolve the debt ceiling issue. This is why it is actually encouraging to see active planning for failure. Given the risk, we should have a plan.

I talked in a previous post about the political options —how the Senate has, twice now, cut a deal with White House approval and essentially dared the House to vote it down. That remains, in my opinion, the most plausible option, but there are others, which range from the serious to the absurd. Let’s start with the serious:

January 9, 2013

There has been a lot of uncertainty in the economy and a lot of volatility in the financial markets. Recently, that has been good; the bump after the fiscal cliff deal took us to a five-year high. Clearly, the expectation in the stock market is that uncertainty has been reduced, problems have been solved, and we have clear sailing ahead.

January 7, 2013

“The tax issue is finished, over, completed.” — Mitch McConnell

“The tax issue is resolved.” — John Boehner

January 4, 2013

I have spent a couple of days talking about the situation in Washington, and now it’s time to take another look at the country as a whole. Despite the fun and games in D.C., the real economy continues to improve in multiple ways. Let’s take a look at some.

First, employment. Today’s data shows that, overall, 155,000 jobs were added in December, just matching population growth. This is a reasonable number that should keep the unemployment rate stable, and that is what happened. Unemployment stayed steady at 7.8 percent, and the underemployment rate (which I prefer) remained stable at 14.4 percent. Not great news, but given the fiscal cliff uncertainty, not terrible either.

{kind=link}

{kind=link}