Print

Print My colleague Sam Millette, senior investment research analyst on Commonwealth’s Investment Management and Research team, has helped me put together this month’s Market Risk Update. Thanks for the assist, Sam!

My colleague Sam Millette, senior investment research analyst on Commonwealth’s Investment Management and Research team, has helped me put together this month’s Market Risk Update. Thanks for the assist, Sam!

Markets continued to rise in August, with both the S&P 500 and Nasdaq Composite setting new all-time highs during the month. The S&P 500 gained 7.19 percent in August, and the Nasdaq and the Dow Jones Industrial Average (DJIA) both saw high single-digit returns as well. Although the continued market rebound in August was certainly welcome, very real risks to markets remain, as we can see when we look at the key factors that matter when determining the overall risk level.

Recession Risk

Recessions are strongly associated with market drawdowns. Indeed, 8 of 10 bear markets have occurred during recessions. As we discussed in this month’s Economic Risk Factor Update, the National Bureau of Economic Research (NBER) declared that a recession started in February. On top of that, most of the major economic indicators we cover monthly remain at a red light, despite continued economic recovery during the month. As such, we have kept the economic factors at a red light for September.

Economic Shock Risk

There are two major systemic factors—the price of oil and the price of money (better known as interest rates)—that drive the economy and the financial markets, and they have a proven ability to derail them. Both have been causal factors in previous bear markets and warrant close attention.

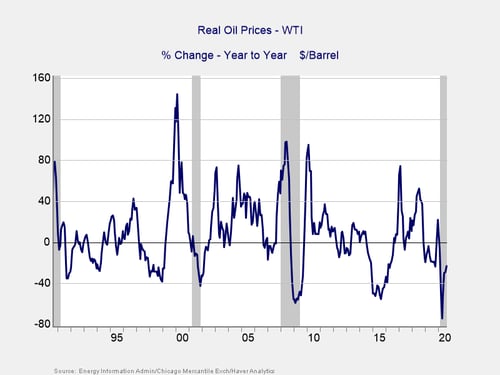

The price of oil. Typically, oil prices cause disruption when they spike. This is a warning sign of both a recession and a bear market. In this case, however, the sudden drop is also a warning of significant disruption.

The price of oil continued to decline notably on a year-over-year basis in August, falling by 22.7 percent. This is not as large of a decline as July’s 29.1 percent drop in prices, but it is still a large decline on a historical basis. Prices rose modestly during the month, from $40.72 per barrel in July to $42.35 per barrel in August. This increase brought the average price of oil to its highest monthly level since February, indicating the sharp drop in prices in April was likely the low-water mark for oil prices in the short term.

Going forward, sustained oil prices at these levels continue to signal a risk, with the energy industry being massively disrupted—as we saw back in 2015. With that being said, the continued recovery in prices in August is a positive development for energy companies, and prices remain low enough to be a boon for consumers.

Despite the positive tailwind that low oil prices create for consumers, we have left this indicator at a red light for now due to the continued double-digit decline in prices on a year-over-year basis and the negative effect that lower prices have on the energy industry.

Signal: Red light

The price of money. We cover interest rates in the economic update, but they warrant a look here as well.

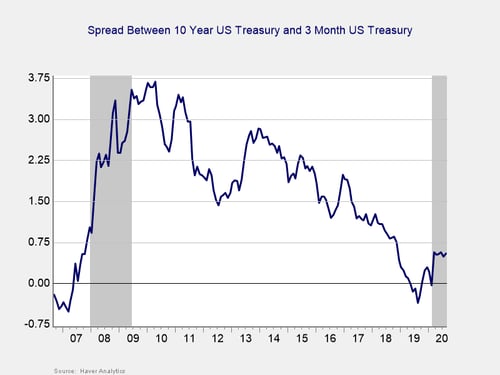

The yield curve started the year inverted, and it un-inverted in March, where it has remained throughout the pandemic. This un-inversion was driven by a sharp drop in short-term rates, which was caused by the Fed’s decision to cut the federal funds rate to effectively zero percent in March. The 3-month Treasury yield rose modestly in August, from 0.10 percent at the start of the month to 0.11 percent at month-end. The 10-year yield also rose, from 0.56 percent to 0.72 percent.

Although an inversion is a good signal of a pending recession, it is when the gap subsequently approaches 75 bps or more that a recession is likely. We finished August with a spread of 61 bps, and the NBER declared a recession started in February. In light of that, and with the spread remaining near the critical level, we are leaving this indicator at a red light.

Signal: Red light

Market Risk

Beyond the economy, we can also learn quite a bit by examining the market itself. For our purposes, two things are important:

- To recognize what factors signal high risk

- To try to determine when those factors signal that risk has become an immediate, rather than theoretical, concern

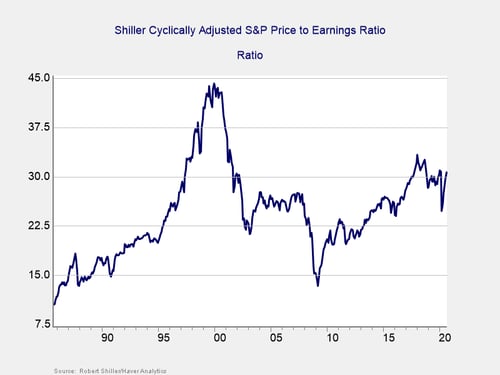

Risk factor #1: Valuation levels. When it comes to assessing valuations, we find longer-term metrics—particularly the cyclically adjusted Shiller P/E ratio, which looks at average earnings over the past 10 years—to be the most useful in determining overall risk.

Valuations increased for the fifth month in a row in August, from 29.6 in July to 30.6 in August. This follows a steep drop to a three-year low of 24.8 in March, at the height of the recent pandemic-driven volatility. Despite the fact that valuations remain below recent highs, risks still remain, given the relatively high valuation from a historical perspective.

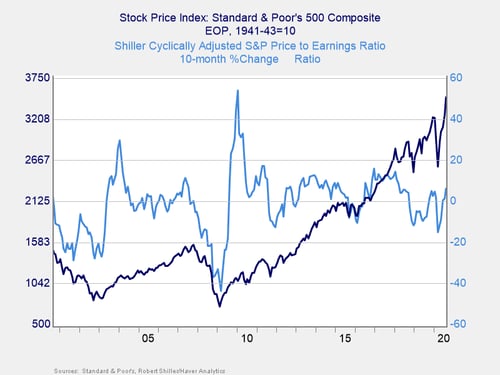

Even as the Shiller P/E ratio is a good risk indicator, it is a terrible timing indicator. To get a better sense of immediate risk, we can turn to the 10-month change in valuations. Looking at changes, rather than absolute levels, gives a sense of the immediate risk level, as turning points often coincide with changes in market trends.

Here, you can see that when valuations roll over, with the change dropping below zero over a 10-month or 200-day period, the market itself typically drops shortly thereafter. This relationship held in March, as valuations and the index both rolled over before rebounding. On a 10-month basis, valuations rose by 6.2 percent, which is the largest increase since 2018. Given the increase in valuations during the month and the historically high valuation levels, we have kept this indicator as a yellow light for now.

Signal: Yellow light

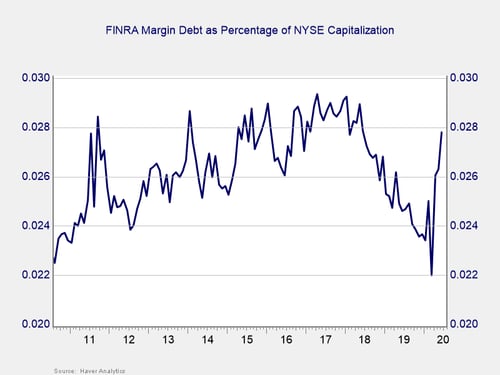

Risk factor #2: Margin debt. Another indicator of potential trouble is margin debt.

Please note: Due to data limitations, the margin debt data is the same data from last month’s update.

Debt levels as a percentage of market capitalization had dropped substantially over the past two years before spiking in February to a six-month high. March saw this measure of market debt fall to levels last seen in 2010, as investors de-risked, before rebounding in April through July along with the market. With the rebound, margin debt remains high on a historical level and is approaching all-time highs seen back in 2017.

For immediate risk, changes in margin debt over a longer period are a better indicator than the level of that debt. Consistent with this, if we look at the change over time, spikes in debt levels typically precede a drawdown.

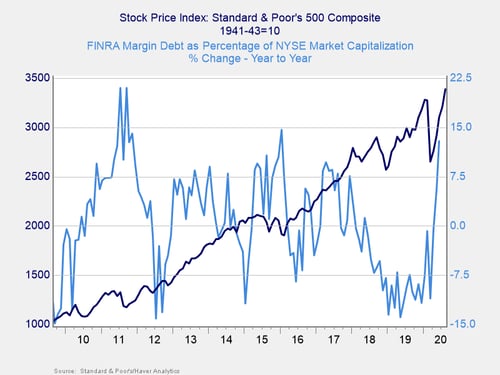

As you can see in the chart above, the annual change in debt as a percentage of market capitalization increased in February, before falling steeply in March and increasing sharply in April through June.

The notable increase in June’s debt levels indicates that risk is rising, as debt increased by 12.9 percent on a year-over-year basis during the month, up from a 5.6 percent annual increase in May. This marks the largest year-over-year increase since January 2016. Given the increase in debt on both a monthly and year-over-year basis, and the fact that the overall debt level remains historically high, this is worth monitoring. So, we are keeping this indicator at a red light.

Signal: Red light

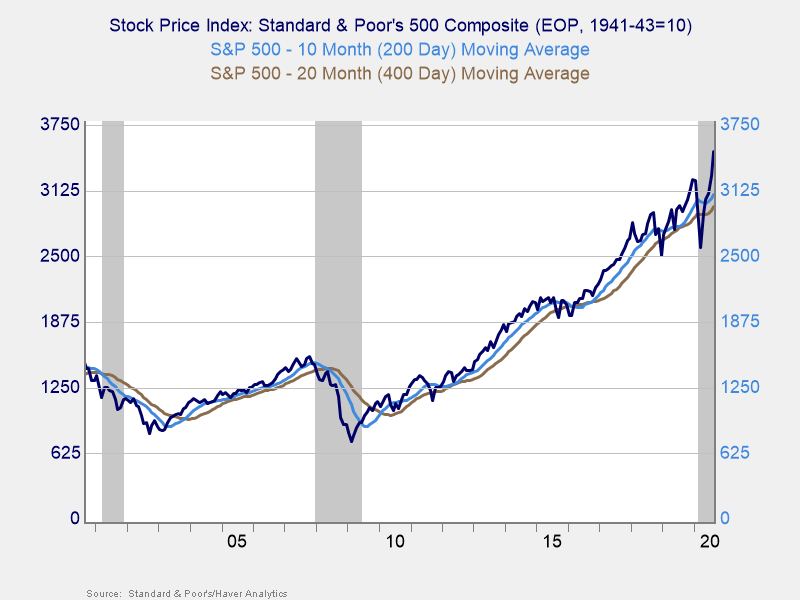

Risk factor #3: Technical factors. A good way to track overall market trends is to review the current level versus recent performance. Two metrics we follow are the 200- and 400-day moving averages. We start to pay attention when a market breaks through its 200-day average, and a break through the 400-day often signals further trouble ahead.

Technical factors were supportive for equity markets in August. The S&P 500, which managed to break above its 200-day moving average at the end of May, finished above trend for the fourth month in a row after spending most of June and all of July and August comfortably above its 200-day moving average. This marks two straight months with all three major indices finishing above trend. The technical support for the DJIA was especially notable, as this was the first month since January where the index spent the entire month above its trendline.

The 200-day trend line is an important technical signal that is widely followed by market participants, as prolonged breaks above or below this trend line could indicate a longer-term shift in investor sentiment for an index. The 400-day trend line is also a reliable indicator of a change in trend. The strong technical support for markets in August was encouraging, so we have left this signal at a green light for the month.

Signal: Green light

Conclusion: Market Risks Remain Despite Continued Rebound

Economic fundamentals showed continued growth in August, albeit at a slower rate than earlier in the summer when reopening efforts and government stimulus provided a tailwind. Markets continued their positive run during the month, highlighting the resiliency of the recent rally. With that being said, the country is not out of the woods yet in terms of containing the virus or fully normalizing the economy, which is what markets are pricing in—leaving them exposed to any setbacks.

Risks to the current market outlook remain, whether in the form of rising case counts or political factors, such as the current social unrest or the upcoming election. Given the multiple red light indicators, rising risks could easily result in more volatility.

As such, and despite signs of improvement, we are keeping the overall market risk indicator at a red light. This is not a sign that markets are necessarily headed back to the lows. Instead, it is a recognition that the road back to normal is likely going to be long, with the potential for setbacks that could lead to additional market pullbacks. Given the uncertainty created by the pandemic and the likelihood for further volatility, investors should remain cautious on equity markets despite recent outperformance.