Print

Print Just as I do with the economy, I review the market each month for warning signs of trouble in the near future. Although valuations are now high—a noted risk factor in past bear markets—markets can stay expensive (or get much more expensive) for years and years, which doesn’t give us much to go on timing-wise.

Just as I do with the economy, I review the market each month for warning signs of trouble in the near future. Although valuations are now high—a noted risk factor in past bear markets—markets can stay expensive (or get much more expensive) for years and years, which doesn’t give us much to go on timing-wise.

Of course, there are other market risk factors beyond valuations. For our purposes, two things are important: (1) to recognize when risk levels are high, and (2) to try and determine when those high risk levels become an immediate, rather than theoretical, concern. This regular update aims to do both.

Risk factor #1: Valuation levels

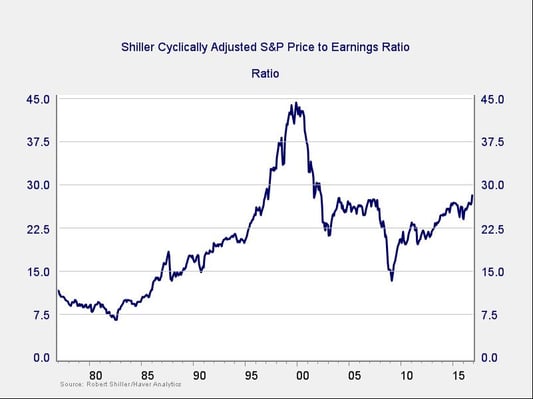

When it comes to assessing valuations, I find longer-term metrics—particularly the cyclically adjusted Shiller P/E ratio, which looks at average earnings over the past 10 years—to be the most useful in determining overall risk.

Two things jump out from this chart. First, after a pullback at the start of 2016, valuations have again risen above levels of 2007–2008 and 2015, where previous drawdowns started. Second, even at the bottom of the recent pullback, valuations were still at levels above any point since the crisis and well above levels before the late 1990s.

Although close to their highest levels over the past 10 years, valuations remain below the 2000 peak, so you might argue that this metric is not suggesting immediate risk. Of course, that assumes we might head back to 2000 bubble conditions, which isn’t exactly reassuring. Risk levels remain high, although not immediate.

Risk factor #2: Changes in valuation levels

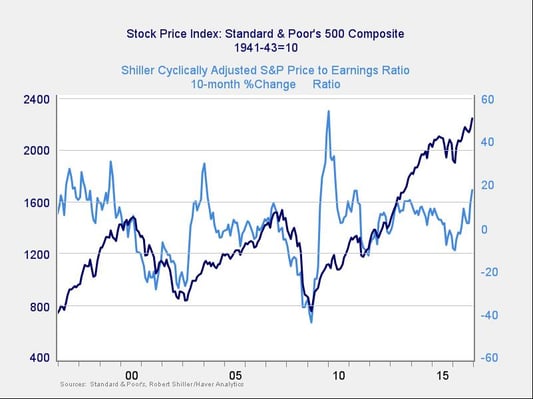

As good as the Shiller P/E ratio is as a risk indicator, it’s a terrible timing indicator. One way to remedy that is to look at changes in valuation levels over time instead of absolute levels.

Here, you can see that when valuations roll over, with the change dropping below zero over a 10-month or 200-day period, the market itself typically drops shortly thereafter. Although we were getting close to a worry point, the recent post-election rally has taken us well out of the trouble zone and into positive territory. Although risks remain, they may not be immediate. Still, this metric will bear watching.

Risk factor #3: Margin debt

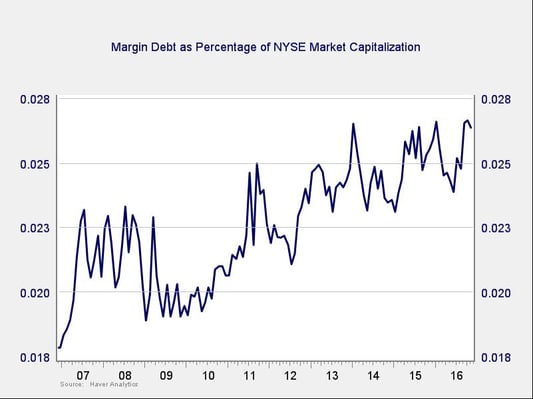

Another indicator of potential trouble is margin debt.

After a decline due to the recovery from the pullback at the start of the year, debt levels have climbed again over the past several months, close to the highest level since the financial crisis. This kind of increase suggests risk levels are rising once again, and the indicator remains high by historical standards. But again, though this metric bears watching, the risk is not necessarily immediate.

Risk factor #4: Changes in margin debt

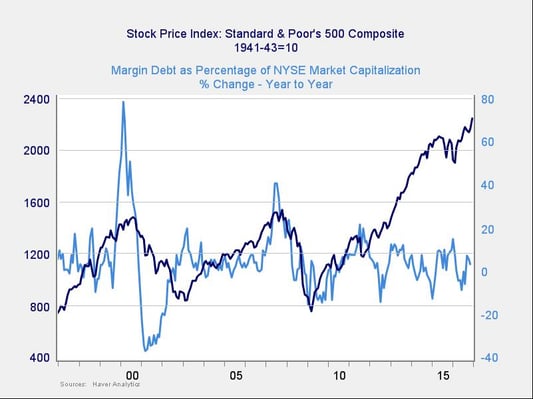

Consistent with this, if we look at the change in margin debt over time, spikes in debt levels typically precede a drawdown.

With the absolute risk level high, the immediate risk level is also rising but has recently turned down. The indicator had been approaching the 10-percent annual increase that suggests risk is becoming more immediate. Overall, though this metric still isn’t at the immediate risk level, it remains close to it.

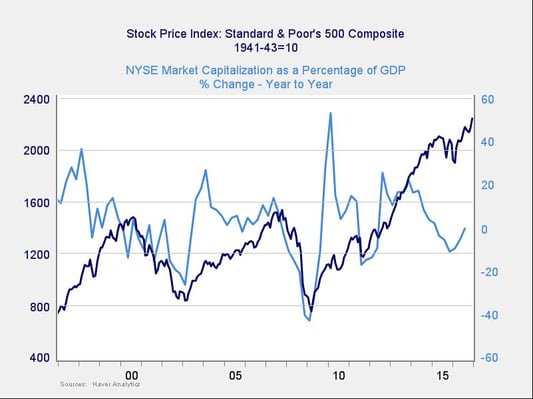

Risk factor #5: The Buffett indicator

Said to be favored by Warren Buffett, the final indicator is the ratio of the value of all the companies in the market to the national economy as a whole.

On an absolute basis, the Buffett indicator has been encouraging. Although it remains high, it had pulled back to less extreme levels. In recent months, however, with the post-election rally, the indicator has started to move back toward the danger zone. Still, we remain some distance from trouble. The recent uptick suggests risks are rising, but they do not seem to be immediate.

Technical metrics are also reasonably encouraging, with all three major U.S. indices well above their 200-day trend lines and close to new highs. With improving sentiment across the board, in consumers, business, and investors, and with rising earnings, it’s quite possible that the advance will continue. Should markets keep rising—and particularly if the Dow hits 20,000—the break into new territory could continue to propel the market higher, despite the high valuation risk level.

On balance, all of the metrics are in what has historically been a high-risk zone, so we should be paying attention. But, as I’ve said many a time, there’s a big difference between high risk and immediate risk—and it is one that’s crucial to investing. As it stands, none of the indicators suggests an immediate problem, although several suggest risk may be rising.