Print

Print Today’s post is from Rob Swanke, senior fixed income analyst on our Investment Management and Research team.

Today’s post is from Rob Swanke, senior fixed income analyst on our Investment Management and Research team.

Generating a yield from your fixed income portfolio has gotten much harder over the past few months. The 10-Year Treasury yield hit a peak of 1.74 percent at the end of the first quarter, but it’s been falling quite steadily since, hitting a low of 1.19 percent on July 19, 2021. Given this drop of more than 0.5 percent over four months, investors who positioned their portfolios for rising rates are likely seeing their performance lag that of the aggregate bond index.

Does the recent yield trend mean rates are going to stay low and inflation is no longer a concern? Not necessarily. But it does provide us with a good view of fixed income’s role in a portfolio. This asset class provides several benefits, which include providing a yield, protecting principal, and diversifying an equity portfolio. So, although the yield bonds provide has fallen, it’s important to keep fixed income’s other benefits in mind. That’s especially true in an environment where rates could rise and inflation is elevated.

What Are Rates Telling Us About the Economy?

After hitting a low of 0.51 percent last August, 10-year Treasury yields started rising in response to an improving growth outlook and increasing inflation expectations. Treasury bonds and, to a lesser extent, corporate bonds lagged the returns of most other asset classes throughout the first quarter. The chart below shows how inflation expectations moved higher over the past year and stayed high (the orange line), even with the fall in Treasury rates (the blue line) since the end of March 2021. The difference between the two data sets (the green line) shows the expected after-inflation yield—aka the real interest rate.

Source: Bloomberg

In the first quarter, we saw growth expectations pick up, based on the vaccine uptake and the waning virus threat. This led to February’s jump in real interest rates, as shown by the green line. In turn, investors rotated away from some high-growth sectors and moved toward more value sectors. But, following the end of the first quarter, this trend reversed. Investors started to anticipate slower growth even though inflation expectations remained high.

Real interest rates are at all-time lows after the recent declines, but this has been a positive for the performance of Treasuries. Even though falling growth expectations haven’t slowed the rise of the S&P 500, a fixed income component in your portfolio could serve as a useful hedge against the potential for slower equity growth ahead. Current fixed income yields could also provide a significant amount of compensation for inflation.

What Role Should Fixed Income Play Now?

Several different economic scenarios could play out going forward. Many economists see an improving picture driven by economies reopening in the U.S. and around the world. This view holds even if other countries are opening at a different pace and may be at more risk related to COVID-19 variants. Fixed income would underperform in an environment of improving economic growth and rising inflation. But it’s important to keep in mind that commodities and/or equities would perform well in this environment. That’s why diversification works. In the long run, equities should outperform all other asset classes. Adding fixed income to a portfolio is meant to reduce volatility, thus bolstering investor confidence in equities for the long term.

Adjustments can always be made to a portfolio in response to different environments. If rates rise due to improving growth expectations, a portfolio with shorter maturities and more credit risk could outperform. If inflation is higher than expected, then a portfolio with Treasury Inflation-Protected Securities (TIPS) could insulate the effects. Conversely, if rates fall as they did during the second quarter, a portfolio with longer-maturity bonds may outperform. The key is understanding the role each investment plays, so you don’t expect it to do something it’s not meant to. This applies to all your assets—it’s not about trying to solve a problem with solely a portfolio’s fixed income allocation.

The Go-To Hedge for Inflation?

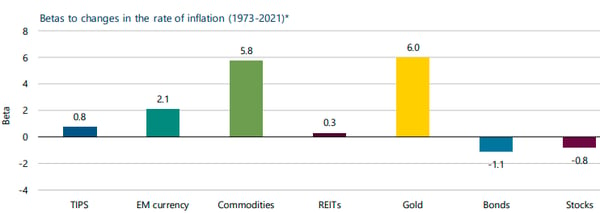

Inflation may be transitory, but it’s still a concern expressed by many investors regarding their fixed income portfolio. The best solution may not be within fixed income. To understand why, let’s look at the chart below, which shows several different asset classes and their sensitivity to changes in the rate of inflation.

Source: PIMCO

TIPS are typically thought of as the go-to hedge for inflation within a fixed income portfolio. But investors could likely get a much better bang for their buck by adding commodities or gold to hedge a portfolio. That’s because these assets are typically a direct cause of inflation. The chart above implies that for a 1 percent increase in the expected rate of inflation, commodities will, on average, have a 5.8 percent return. But TIPS would provide a return just high enough to offset the inflation increase. So, if you’re concerned with inflation, adding a small amount of commodities could potentially protect a much larger portion of your portfolio than adding TIPS.

Looking at Historical Value

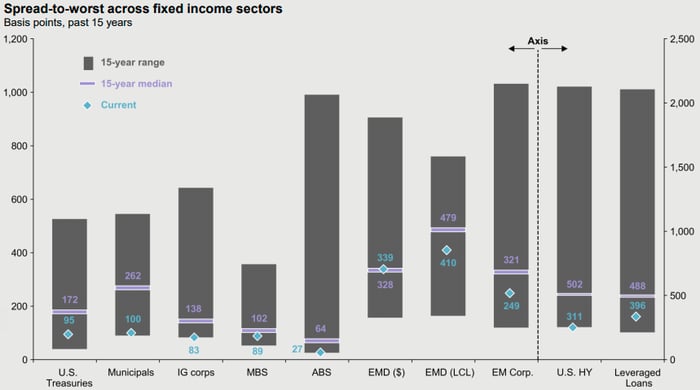

When thinking about allocations within your fixed income portfolio, it’s wise to look at value relative to history. As shown in the chart below, nearly every fixed income asset class has valuations close to its historical highs. That’s understandable given the Fed’s supportive policies and our improving outlook for economic growth. The blue diamonds indicate how much additional yield over Treasuries each asset class pays relative to its historical median (the purple line). Notably, one asset class that still has valuations close to its historical median is emerging markets debt (the EMD column).

The data shows that emerging markets debt can provide a significant boost in yield as well as a diversified source of return and a hedge against inflation. Nonetheless, this sector comes with higher risk due to the threat of the virus and geopolitical factors. Given the risks, investors might be wise to consider emerging markets debt as only a satellite position in a portfolio.

What Fixed Income Is Meant to Do

The core of your fixed income portfolio should consist of high-quality bonds that provide the diversification from equities that fixed income is supposed to provide. There is still a place for high yield or leveraged loans, which can provide some additional yield for a portfolio, especially in a good economic environment. But these types of debt typically show more correlation with equities, which reduces their diversification benefits. When thinking about moving toward higher-risk fixed income allocation, remember what your fixed income portfolio is meant to do. As a New Englander, when thinking about how to allocate to fixed income I like to focus on something Patriots coach Bill Belichick says: “Do your job.”

Treasury Inflation-Protected Securities (TIPS) are inflation-linked securities issued by the U.S. government whose principal value is adjusted periodically in accordance with the rise and fall in the inflation rate. Thus, the dividend amount payable is also affected by variations in the inflation rate, as it is based upon the principal value of the bond. It may fluctuate up or down. Repayment at maturity is guaranteed by the U.S. government and may be adjusted for inflation to become the greater of the original face amount at issuance or that face amount plus an adjustment for inflation.

Bonds are subject to availability and market conditions; some have call features that may affect income. Bond prices and yields are inversely related: when the price goes up, the yield goes down, and vice versa. Market risk is a consideration if sold or redeemed prior to maturity.