Print

Print Throughout the pandemic, we’ve seen a large-scale exercise in risk assessment. Both governments and individuals have had to make a number of risk assessments, weighing the cost and benefits of different actions without definitive information. Investors are making investment decisions based on risk as well, as no one can be a perfect forecaster. So, to the extent we can, we must not only be conscious of the uncertainty of our investment returns but also of the risk that we will make poor choices when faced with different results, both good and bad.

Throughout the pandemic, we’ve seen a large-scale exercise in risk assessment. Both governments and individuals have had to make a number of risk assessments, weighing the cost and benefits of different actions without definitive information. Investors are making investment decisions based on risk as well, as no one can be a perfect forecaster. So, to the extent we can, we must not only be conscious of the uncertainty of our investment returns but also of the risk that we will make poor choices when faced with different results, both good and bad.

One of the biggest problems when evaluating decisions that are based on probabilistic outcomes is that we overestimate our ability to take risk and change our decisions based on recent outcomes, even if they have a low probability.

A Roll of the Dice

To demonstrate, let’s play a game. You have $100 to play either game 1 or game 2.

- In game 1, you get to roll two dice. If you roll a 3, 4, or 5, you lose. But if you roll anything else, you win. In other words, you have a 75 percent chance to win.

- In game 2, you get to roll two dice. If you roll an 8, 9, or 10, you lose. But if you roll anything else, you win. Here, you have a 66 percent chance to win.

Choosing game 1 is an easy decision for most. So, let’s make it a bit more challenging. To play game 1, you must roll 6 times and bet the entire amount you have each time. If you have nothing left, the game is over. In game 2, you bet only half of what you have each time. Now, which game would you choose?

Investment Risks and Returns

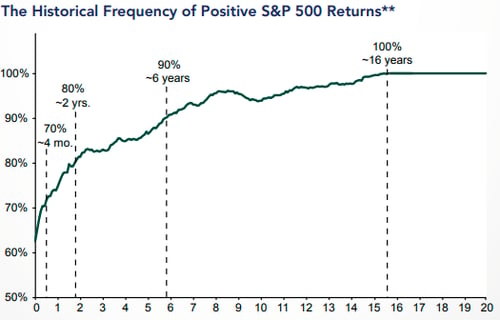

Before I tell you how the distribution plays out, let’s think about how this scenario applies to investing. In general, equity markets move higher, more often than not, on an annual basis. On a rolling 1-year basis, the S&P 500 moves higher nearly 75 percent of the time. Moving out to longer time frames, the S&P 500 moves higher 87.5 percent of the time over a 5-year rolling time frame and 94 percent of the time over a 10-year rolling period.

Source: Fisher Investments, Global Financial Data, Inc. as of 12/31/2017. **Plots the percentage of positive S&P 500 rolling periods (from 0 to 20 years), showing longer time frames significantly increase the frequency of positive stock market returns. Calculated using monthly rolling holding periods from 1/31/1926 to 12/31/2017.

In that same regard, the average return of the S&P 500 is much higher than that of fixed income. Given that the S&P 500 goes higher most of the time and produces higher returns, why choose to invest in fixed income?

One of the biggest reasons is risk management. We certainly can’t emphasize enough the impact fixed income has on reducing the volatility of a portfolio and diversifying equities. But it can also help you avoid the risk of making poor decisions in the future by helping you maintain confidence in your portfolio as a whole. As investors, we all have unique tolerances for risk, and we must be cognizant of that fact. If the market declines 20 percent and that causes you to move out of equities, you will likely lose out on future appreciation and, more importantly, fail to achieve your investment goals.

Evaluating the Results

Moving back to our game, which option did you choose? You may notice I didn’t say how you won the game. In essence, everyone had to choose what it meant to win. Game 1 is the winner for the highest expected value ($1,132) and the highest possible winnings ($6,400). Game 2 had a lower expected value ($256) but would end up with the higher amount more often than game 1 since you would never lose your entire balance. In game 1, you would end up with a total loss 82 percent of the time. A third way to look at it would be the chance of reaching a certain target. If you had a $500 target, then game 2 only reaches that target 9 percent of the time, while game 1 reaches it 18 percent of the time. If you had a $200 target, then game 1 only reaches it 18 percent of the time while game 2 reaches the target 36 percent of the time. When investing, it’s important to set goals, because it helps determine how much risk you are taking to reach those goals.

Our Current Environment

With inflation running high and yields low, many are tempted to move out of fixed income and into equities. For some, this may make sense depending on their goals. For others, however, increasing the risk profile of their portfolio may cause them to have a lower probability of reaching their goals. In game 1, players ended up with nothing 82 percent of the time because they continually risked their entire bankroll and couldn’t continue to play a game that had a 75 percent chance of success because they ran out of money. In a similar manner, fixed income helps ensure that your portfolio can withstand losses and that you can remain invested in equities, giving you the opportunity to rebalance your portfolio when equity results aren’t in your favor.

In investing, unlike in the game, you aren’t forced to continually bet your entire portfolio, nor are the odds of success in any given year the same. This can actually make achieving success more difficult, since it adds more variables to the equation, giving you more opportunities to make an error. Using target allocations to fixed income and equity can help keep your portfolio grounded and keep you from making decisions that cause you to chase returns or move to cash when markets are volatile.

It’s been more than 12 years since the S&P 500 has had a calendar year loss greater than 5 percent and almost 20 years since we’ve had consecutive calendar year losses. As we move further away from those losses, people may discount the risks of a large or protracted decline in equity markets and seek to move away from their targets to take on higher risks in the face of lower expected returns. The important thing to ask yourself is if the dice come up on the wrong end, will you still be able to play the game?