Print

Print The big news this past week has been what has not happened: there are, at present, no signs of a second wave of infections stemming from the ongoing reopening of the economy and the loosening of social distancing measures in several states. In fact, the data shows that social distancing had been subsiding in many areas even before the formal loosening. So, we are now two weeks or more into the start of a new environment for the spread of the virus. While it is still early in the process, some growth in cases could have been expected. The fact that we have continued to see the spread rates at close to the lowest levels of the pandemic is positive.

The big news this past week has been what has not happened: there are, at present, no signs of a second wave of infections stemming from the ongoing reopening of the economy and the loosening of social distancing measures in several states. In fact, the data shows that social distancing had been subsiding in many areas even before the formal loosening. So, we are now two weeks or more into the start of a new environment for the spread of the virus. While it is still early in the process, some growth in cases could have been expected. The fact that we have continued to see the spread rates at close to the lowest levels of the pandemic is positive.

In more good news, the reopening seems to be proceeding faster than expected as consumers move back into the economy. Mobility and restaurant demand have come back much faster than expected, mortgage applications are back to levels of last year, while consumer and business confidence appear to have bottomed and started to recover.

The news around testing is more mixed. Questions were raised last week about what has been included in the reported test figures, from both the Centers for Disease Control and Prevention and a number of states, with the implication that the numbers had been meaningfully overstated. The recent decline in the number of tests reported suggests that is indeed the case but that those numbers are now being more reliably reported. Even given the lower number of reported tests, the rate of positive tests remains low, which suggests the data continues to trend favorably.

Overall, conditions remain much better than a couple of weeks ago and suggest that, so far, the reopening is proceeding smoothly from both a medical and economic perspective. Let’s take a look at the details.

Pandemic growth remains slow

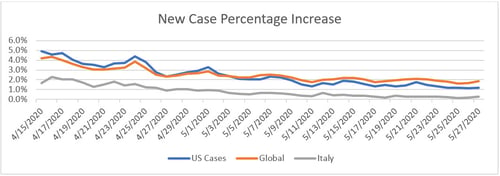

Growth rate. Over the past month, the new case growth rate has declined from about 5 percent per day to the present level of less than 2 percent per day. Over the past two weeks, however, the growth rate has been consistently under 1.5 percent per day, which is modest progress. If that growth rate holds, the number of cases will double about every seven weeks. We have succeeded in flattening the curve, but the virus continues to spread. Given the reopening of the economy, however, this is good news in that we have not seen any significant increase over the past couple of weeks.

Source: Data from worldometer.com

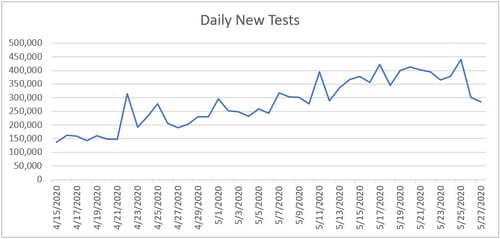

Daily testing rate. Testing rates dropped off in recent days, likely as states are limiting the number of tests reported to only those indicating new infections. This change is in response to recent news stories questioning the prior practice of also including antibody tests, which indicate past exposure rather than current infection. While the number of tests is declining, the data going forward should be more accurate.

Source: Data from the COVID Tracking Project

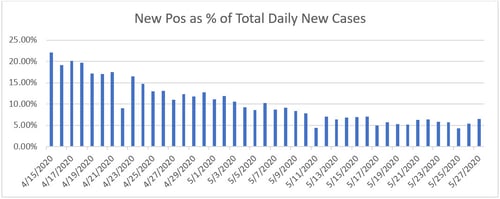

Positive test results. Another way of seeing this progress is to look at the percentage of each day’s tests that are positive. Ideally, this number would be low, as we want to be testing everyone and not just those who are obviously sick. The lower this number gets, the wider the testing is getting. Here, we can see that despite the decline in the number of tests reported, the positive level remains low. This result suggests that we still have enough tests in place, even at the lower level, to get a reasonable grasp of how the pandemic is spreading.

Source: Data from the COVID Tracking Project

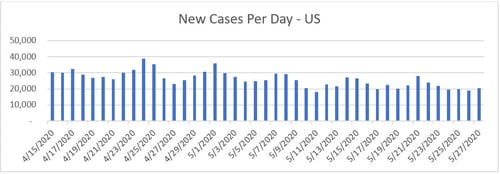

New cases per day. Despite the reopening and the decline in testing, the number of new cases per day has remained steady, at around 20,000 per day. This number is, again, somewhat better than it looks. With the reopening, other things being equal, we would expect reported cases to increase—which has not happened. Stabilization, in this context, continues to be positive overall.

Source: Data from worldometer.com

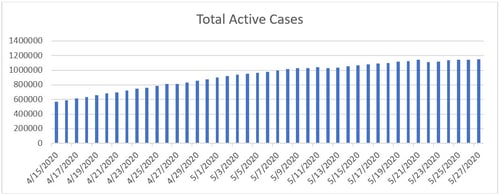

Total active cases. Active case growth also continues to moderate, with under 10,000 per day for the past three days and with almost no increase over the past week.

Source: Data from worldometer.com

Overall, the pandemic continues to be largely under control, with no signs yet of a major second wave of infections despite the reopening. This possibility remains something we need to watch. But overall and given the reopening, the news on the pandemic front is still quite positive.

Peak economic damage behind us

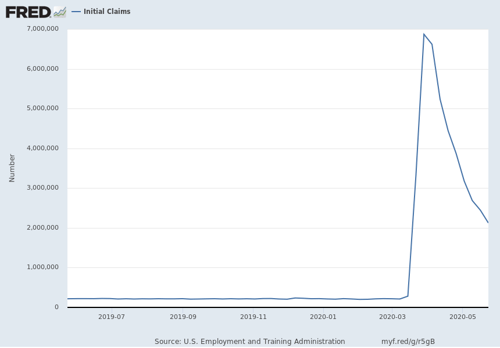

Jobs market. While layoffs continue, there are signs that the damage may have peaked and has started to recede. Weekly initial unemployment claims continue to decline from the peak, suggesting that much of the damage has already been done.

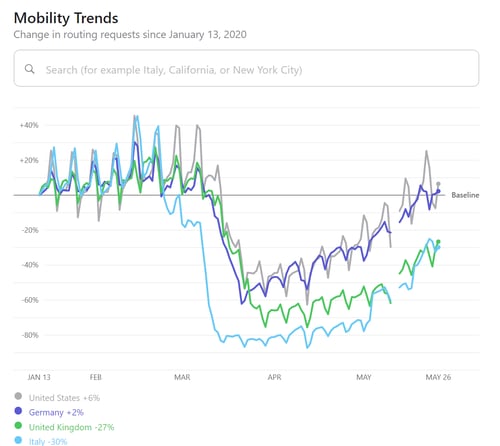

With the lockdown easing, Apple mobility data has bounced back and is now above the level of early March. This bounce is a significant improvement, suggesting people are now coming out of their homes again. We also see this improvement in one of the hardest hit areas of the economy, restaurants, which have started to come back in many areas. There is still a long way to go, but the process has started.

Source: apple.com

The risks. Although the reopening is going better than expected and is clearly having some positive economic effects, as we reopen we certainly face risks. The biggest of these is a second large wave of the pandemic. We have not seen that yet, though, which is a positive sign, suggesting that most people are continuing to act in a safe manner.

Another potential risk is that, even with the reopening, consumers will be slow to return and spending growth will not return to what was normal any time soon. This outcome seems possible, although the early signs are positive, with restaurants coming back faster than expected. Another positive sign is that mortgage applications are almost back to 2019 levels, which would drive additional spending, and Google searches for vehicle sales have rebounded significantly. While risk of a slow spending recovery still exists, early data shows that spending might come back faster than anyone expected.

Markets reassessing the risks

For the financial markets, now that the reopening is underway, markets have been reassessing the risks, and we have seen some volatility. While that risk remains, the good news is that as we get that data, markets will have a much firmer foundation. The past week’s data has been positive on the whole, and markets have responded—a trend that will likely continue if the news remains positive.

What’s the takeaway?

The real takeaway from this past week is that progress continues, to the point that a continued successful reopening over the next several weeks looks likely unless something significant changes. We are not yet out of the woods, and there are certainly significant risks going forward—with a second wave of infections being the biggest. But the thing to keep in mind is that many of the biggest risks are moving behind us. Another good week.