Today, President Obama and Speaker Boehner, along with their teams, will sit down at the White House to try and figure out how to solve this thing. Encouragingly, everyone seems to be shutting up.

November 16, 2012

Today, President Obama and Speaker Boehner, along with their teams, will sit down at the White House to try and figure out how to solve this thing. Encouragingly, everyone seems to be shutting up.

November 14, 2012

Remember when I said we would see more volatility as the negotiations played out in the press? Today’s front-page article in the Wall Street Journal (WSJ), “Obama Sets Steep Tax Target,” discusses how the President is using his proposed budget, with $1.6 trillion in additional revenue, as a starting bid. This is twice the additional revenue that he and Boehner were talking about in their last set of negotiations and is a nonstarter from the Republicans’ point of view. Surprise—stocks are down again this morning.

Obama is also reported to be under pressure from the left on the budget. Yesterday’s WSJ had “Labor Pressures Obama on Budget” on page A6, which was confirmed in today’s New York Times (NYT) with “Obama Tells Labor Chiefs He Won’t Yield on Budget.” Earlier this week, we saw the Republicans playing to their base; now we see the same with the Democrats.

November 6, 2012

So here we are, Election Day, and the uncertainty will soon be resolved. Right?

October 29, 2012

The good news is that GDP growth came in a bit better than expected—at 2 percent versus 1.8 percent, which is up from 1.3 percent in the previous quarter. This was front-page news in the weekend editions of the New York Times (NYT) and the Wall Street Journal (WSJ). For the first time in two years, government spending was a major driver of growth. Consumer spending was also a significant contributor, but it came at the cost of lower saving rates, so it may not be sustainable. Business investment dropped, as did exports, in the face of growing weakness in Europe and China.

The sustainability of the growth is questionable, given that government spending is very likely to decrease going forward; in addition, consumer spending is also likely to slow (at best) as the fiscal cliff tax increases come closer. Nonetheless, a good quarter.

October 26, 2012

There is a fair bit of news today, which I will deal with in other posts, but I wanted to start with this one because I think it encapsulates a lot of the arguments that are being made at a national level.

October 25, 2012

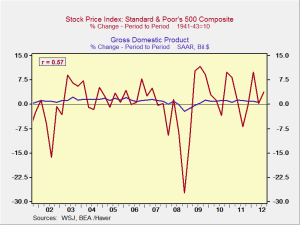

Over periods of time, the performance of the stock market and the real economy are closely linked. This is no surprise; in fact, it’s inevitable if you think about it, as the stock market is just the business expression of the real economy. The correlation of changes in the two has been about 60 percent over the past decade, meaning that the majority of the changes in the stock market can be explained by changes in the size of the real economy.

October 24, 2012

“Standing in the middle of the road is very dangerous; you get knocked down by the traffic from both sides.” — Margaret Thatcher

Margaret Thatcher is not usually associated with the middle of the road, but I have always liked the above quote. And, indeed, there is no question that the middle of the road may be the place to be in American politics.

October 23, 2012

I sent a tweet about this earlier, but I want to mention it here as well. This Wall Street Journal article by Daniel Yergin, “The Real Stimulus: Low-Cost Natural Gas,” is worth a read.

The title pretty much tells the story, but Yergin goes into some detail about the numbers behind the story, as well as some of the second-order repercussions.

The market is a beautiful thing. Money flows to what people want, and the end result is that the optimal balance of desires and available resources is obtained with minimal guidance and intervention.

October 22, 2012

All right, we did the optimism thing last week—now, back to the regular program. Not quite as bad as that, of course, but last Friday was the 25th anniversary of the 1987 crash, and that has focused minds a bit.

The anniversary of the crash hit the papers last Friday and over the weekend, with “Unhappy Anniversary, Dow” in the weekend Wall Street Journal (WSJ) followed by “That Old Sinking Feeling Returns, Circa October 1987” (p. B1 and p. B5, respectively). These articles were supported by “It’s Time to Time the Market” (WSJ, p. B7), which is about how the market is priced at a level that historically has produced disappointing returns going forward. I will note that my own research, as well as that of many others, also supports the conclusions of that article. The New York Times (NYT) didn’t explicitly headline the crash, but it did put “Shares Fall as Earnings Disappoint on Wall St.” on B1, the front business page.

{kind=link}