Print

Print The news over this past week is what has still not happened: at present, there are no signs of a second wave of infections stemming from the ongoing reopening of the economy and the loosening of social distancing measures in several states. In fact, the data shows that social distancing had been subsiding in many areas even before the formal loosening. So, we are now three weeks or more into the start of a new environment for the spread of the virus. Not only has there been no significant increase in the case growth rate, but case growth itself has trended back down to around 20,000 per day.

The news over this past week is what has still not happened: at present, there are no signs of a second wave of infections stemming from the ongoing reopening of the economy and the loosening of social distancing measures in several states. In fact, the data shows that social distancing had been subsiding in many areas even before the formal loosening. So, we are now three weeks or more into the start of a new environment for the spread of the virus. Not only has there been no significant increase in the case growth rate, but case growth itself has trended back down to around 20,000 per day.

The real question now is whether recent public protests will generate another wave of infections. We won’t know the answer for at least another two weeks, but this possibility is something we must keep an eye on through June.

In other good news, the reopening is still on track as consumers move back into the economy. Mobility and restaurant demand have continued their substantial improvement, and auto sales have bounced back strongly. Plus, consumer and business confidence appear to have bottomed and started to recover.

After a slowdown in testing growth, as well as questions about the underlying data, the news here was better than last week. Testing moved back up and the rate of positive tests stayed low, suggesting that the data continues to trend favorably.

Overall, conditions continue to improve, although at a slower rate. So far, the reopening is proceeding smoothly from both a medical and economic perspective. Let’s take a look at the details.

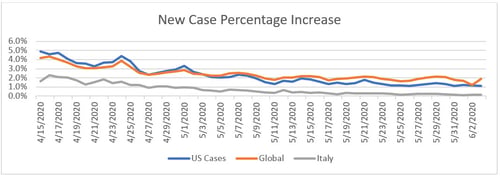

Pandemic growth remains slow

Growth rate. Over the past 10 days, the growth rate has held between 1.1 percent and 1.4 percent per day, with most in the 1.1−1.2 percent range. At this rate, the curve has been flattened. If that growth rate holds, the number of cases will double about every eight to nine weeks. While the virus continues to spread slowly, given the reopening of the economy, this slow growth rate is good news in that we have not seen any significant increase over the past couple of weeks.

Source: Data from worldometer.com

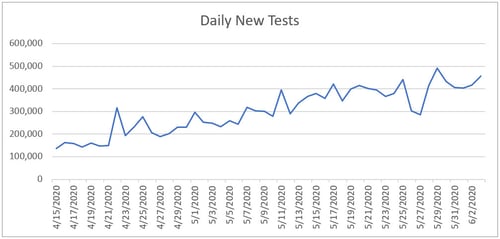

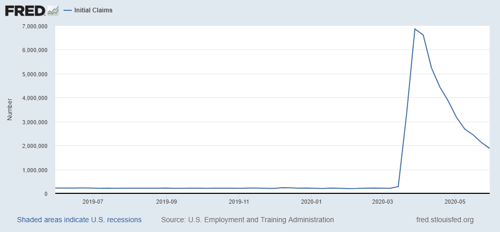

Daily testing rate. After a drop, testing rates have recovered in past days and look to be increasing steadily. We have seen slowdowns like this before, and the recovery suggests this rate should continue to improve in coming weeks.

Source: Data from the COVID Tracking Project

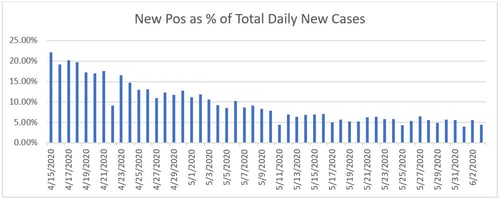

Positive test results. Another way of seeing this progress is to look at the percentage of each day’s tests that are positive. Ideally, this number would be low, as we want to be testing everyone and not just those who are obviously sick. The lower this number gets, the wider the testing is getting. Here, we can see that the positive level remains low, suggesting that we are getting to the point of having enough tests in place to get a reasonable grasp of how the pandemic is spreading.

Source: Data from the COVID Tracking Project

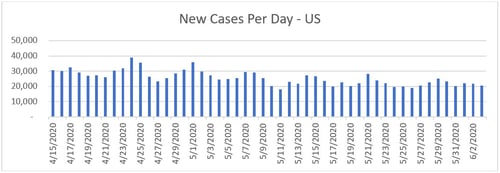

New cases per day. Despite the reopening, the number of new cases per day has declined again, after a brief bump, to around 20,000 per day. This number is, again, somewhat better than it looks. With the reopening, other things being equal, we would expect reported cases to increase—which has not happened. Stabilization, in this context, continues to be positive overall.

Source: Data from worldometer.com

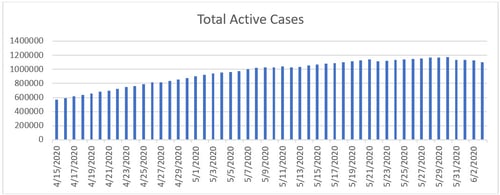

Total active cases. Active case growth has shown the most improvement in the past week and may actually have reached a peak, as case resolutions now exceed new infections on many days. This improvement is another sign that we have successfully flattened the curve.

Source: Data from worldometer.com

Overall, the pandemic continues to be largely under control, with no signs yet of a major second wave of infections despite the reopening. This possibility remains something we need to watch for, especially given the risks imposed by the protests. Still, given the reopening, the news on the pandemic front remains quite positive.

The economy bottomed in April

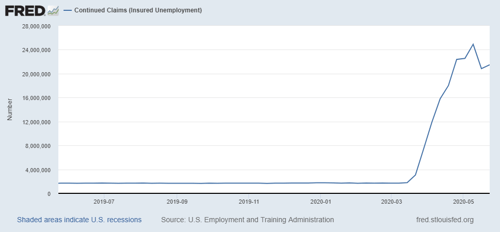

Jobs market. While layoffs continue, there are signs that the damage may have peaked and has started to recede. Weekly initial unemployment claims continue to decline from the peak, suggesting that much of the damage has already been done.

Continuing unemployment claims also seem to have peaked and actually declined last week, suggesting many people are starting to move back to work. Also supporting this idea was the most recent jobs report from ADP (a large payroll company). It showed 2.76 million jobs lost, down from 20.236 million jobs lost in the prior report and well below the 9 million expected. As this report represents actual payrolls, it is a solid indicator that the job market is now improving.

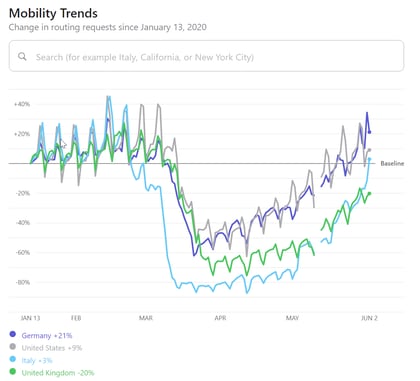

Consumers on the move. With the lockdown easing, Apple mobility data has continued to trend higher and is now above the level of early March. This jump is a significant improvement, suggesting people are now coming out of their homes again. We also see this improvement in one of the hardest hit areas of the economy, restaurants, which have started to come back in many areas. There is still a long way to go, but the process has started. Consumers are also buying autos again, with a significant bounce in sales last month.

Source: apple.com

The risks. Although the reopening is going better than expected and is clearly having some positive economic effects, we certainly face risks. The biggest of these is a second large wave of infections. We have not seen that yet, which is a positive sign, as it suggests that most people are continuing to act in a safe manner. That said, the recent protests have significantly increased the risk of a second wave.

Another potential risk is that, even with the reopening, consumers will be slow to return and spending growth will not return to what was normal any time soon. This outcome seems possible, although the early signs remain positive, as restaurants continue to come back faster than expected. Another positive sign is that auto sales have rebounded significantly. While risk of a slow spending recovery still exists, the data so far shows that spending is coming back at a substantial pace.

Positive market trends

Now that the reopening is underway, financial markets have been reassessing the risks, and we have seen some volatility. While that risk remains, the good news is that as we get that data, markets will have a much firmer foundation. The past two weeks of data has been positive on the whole, and markets have responded—a trend that will likely continue if the news remains positive.

Another good week

The real takeaway from this past week is that progress continues, to the point that a continued successful reopening over the next several weeks looks likely unless something significant changes. We are not yet out of the woods, and there are certainly significant risks going forward—with a second wave of infections from the protests being the most significant. But the thing to keep in mind is that many of the biggest risks are moving behind us.