Print

Print As fiduciaries, advisors are tasked with putting client interests ahead of their own. They have a duty to preserve good faith and trust. From an investment perspective, that includes considering all materially relevant information to mitigate risk and improve returns through prudent investment management. But from an environmental, social, and governance (ESG) investing perspective? It’s where the rift between proponents and opponents of this investing strategy begins.

As fiduciaries, advisors are tasked with putting client interests ahead of their own. They have a duty to preserve good faith and trust. From an investment perspective, that includes considering all materially relevant information to mitigate risk and improve returns through prudent investment management. But from an environmental, social, and governance (ESG) investing perspective? It’s where the rift between proponents and opponents of this investing strategy begins.

Unpacking the ESG Debate

Proponents believe that ESG metrics need to be considered because they help inform and enhance the investment decision-making process. They also think company management should consider ESG principles because they help firms prepare and position for a rapidly changing world.

Opponents, on the other hand, argue that the incorporation of ESG principles hinders profit potential by burdening investors, boardrooms, and company management with unnecessary nonfinancial considerations that aren’t tied to the bottom line.

In other words, ESG has fallen into an ideological tug-of-war. In many cases, the space is being redefined into something that is completely at odds with its original core principles. To be sure, the media has done an excellent job of stoking the ESG fire, often using it to their advantage to sell advertising space or drum up support for a particular agenda. As a result, investors have been left without a clear understanding of how ESG is being used in practice.

To provide some clarity and understanding of ESG and its underpinnings, let’s start with a look back at the industrial and post-industrial worlds, particularly as they relate to firm value and competitive advantage.

Firm Valuation: Intangible Vs. Tangible Assets

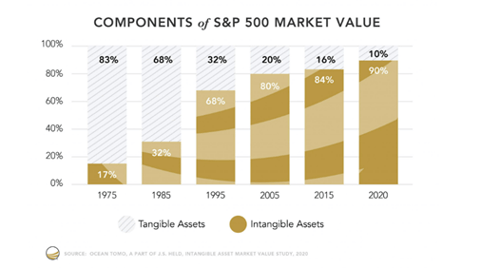

For the better part of the 20th century, firm valuation was largely dependent on tangible items (e.g., property, plant, and equipment). In 1985, roughly two-thirds of the S&P 500 market value was made up of tangible assets (see chart below), and only one-third came from intangibles. A business’s net worth and core operations were highly dependent on its assets, which is why investors paid little attention to things like brand reputation. In that climate, traditional security analysis with a focus on financial ratios and metrics worked exceptionally well because a company’s net value was clearly defined through the tangible. Investors, therefore, didn’t really need to concern themselves with “nonfinancial” considerations like goodwill and employee satisfaction.

Fast-forward 35 years and intangibles now dominate firm value to the point where tangibles have almost become an afterthought. In today’s environment, a firm’s brand and reputation carry more value than the goods on its shelves or equipment in its warehouses. Further, a firm’s relationships with customers, employees, suppliers, and communities have never been more important. Firm value has changed over the decades—which means investing styles have, too. So, how did we get here?

An Evolving Corporate Landscape

For the better part of the past 40 years, firms have spent little time worrying about employee satisfaction levels, fringe benefits, and perks because the labor supply was plentiful. Women were increasingly entering the workforce, and the baby boomer generation helped match supply with demand. In many cases, it wasn’t uncommon for employees to spend their entire career at the same firm because the barriers to switching companies or careers were high, which typically involved physically relocating.

Today, the labor supply is exceptionally tight, and the widespread use of remote work means that workers can switch careers or jobs quite easily, often without physically moving. Negotiating power has swung from employer to employee, and turnover rates and wages have skyrocketed as a result. Firms are now implementing unique strategies to attract and retain top talent because increased turnover, in any industry, is costly to the bottom line. It’s also damaging to culture and productivity. Therefore, nonfinancial metrics like employee satisfaction scores and turnover rates are becoming more important to investors (and company management) than ever before.

Brand Loyalty Reigns Supreme

Firm reputation and brand loyalty have become paramount from a valuation perspective thanks to the internet, smartphones, and social media. At the click of a button, individuals can send out reviews, tweets, and posts to millions of followers, which can influence a brand’s image in the eyes of the consumer. Everyday product reviewers and social media influencers have become integral components of the brand landscape.

Online shopping means that customers have more options than ever before, and they’re very willing to quickly move on if companies abuse their trust. It’s why firms are spending vast amounts of money on advertising to gain and retain customer loyalty, while striving to appeal to a broadly diversifying customer base. As a result, it’s no longer a consumer-beware culture. Instead, brand loyalty has become a key focus for company management and investors in recent years.

The New Economy

It’s evident that the corporate climate and firm valuation have changed, and investment analysis has evolved along with it. Historically, investors didn’t concern themselves with intangible criteria because firms operated in a tangible world. There was no need to consider things like employee satisfaction scores and turnover ratios, or whether a company’s products were engendering appropriate loyalty from consumers across ever-changing demographic channels.

Today, investors want to know whether there are legal claims outstanding or if legacy environmental issues will require a significant investment to modernize facilities. From a governance perspective, they want to understand the firm’s data privacy policies, make sure there’s an audit committee in place, and gain an understanding of the board oversight structure.

These types of questions are being asked because they are more material to the bottom line than ever before. They can help expose risks that may not show up in profitability numbers until it’s too late (e.g., Enron, Volkswagen, and BP). These types of questions and metrics would be described as ESG; as such, some argue they should not be considered. But in taking that approach, ESG opponents would be casting aside meaningful, materially relevant information that could be the difference between a great stock and one that’s fraught with controversy or fraud.

Is It Time to Change the Narrative?

It’s clear ESG has become an ideological hot button. But what if we changed the narrative and called it SMART investing (specific, measurable, accountable, relevant, and timely)? Putting politics aside, it’s hard to argue that there’s little value in material nonfinancial information that provides a well-rounded view of company management and operations, particularly in a world that is more intangible than ever before.

As stewards of $206 billion in client capital (as of October 25, 2022), our job here at Commonwealth is to see through the noise by maintaining an independent, objective view for allocating client capital. It extends to the tools, resources, and information available that will enable us to reduce risk while improving returns. Ignoring accessible, materially relevant information is not only imprudent, but it goes against one’s fiduciary responsibility. Therefore, whether you call it SMART investing or ESG, there’s value to be had from an approach that seeks out an informational advantage in a nontraditional way. I think we can all agree on that.