Print

Print Today’s post on ESG investing comes from Brian Price, senior vice president of investment management and research here at Commonwealth—and a self-proclaimed ESG investing skeptic. Over to you, Brian!

Today’s post on ESG investing comes from Brian Price, senior vice president of investment management and research here at Commonwealth—and a self-proclaimed ESG investing skeptic. Over to you, Brian!

In the early days of my career as a research analyst, I was taught to approach new investment styles and themes with a healthy dose of skepticism. After all, many fads come and go, and very rarely does a concept get introduced that will have a profound difference on the way that clients invest their money. This background may help explain why the concept of socially responsible investing (SRI) was one that I didn’t fully appreciate back then. Specifically, I had a hard time accepting the fact that this investing style would ever be embraced by anyone except those whose investment decisions were seemingly guided by their desire to save the environment. Looking back, I realize that this was a narrow-minded view and that SRI is not only a way for people to choose to invest, it may also become a part of the way we all invest.

From SRI to ESG

To start, let’s address the evolution of SRI over the past five years. To briefly summarize, SRI has evolved to include a growing emphasis on corporate governance in the investment process. That accounts for the G in ESG (environmental, social, and governance) investing—evaluating how companies are making money and who is benefiting most from those profits.

The transition from SRI to ESG investing was important, but I wasn’t sure it would be enough for the style to become widely adopted by retail and institutional investors in the U.S. I believed that in the absence of a true commitment from investors, asset flows would never be significant enough to encourage asset management companies to launch investment products. In short, I doubted the ability to create a virtuous circle of ESG adoption that was necessary for success.

ESG goes mainstream

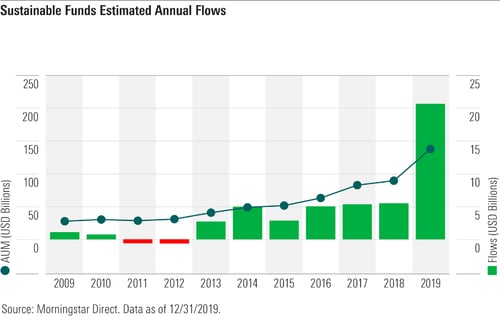

As it turns out, I clearly underestimated that commitment. As the chart below illustrates, asset flows into ESG mutual funds and ETFs had been steady for much of the past five years before skyrocketing in 2019. There was no watershed moment that caused this surge, but it did put the industry on notice. ESG investing had evolved into anything but a fad and appeared, in fact, to have become a permanent fixture in the investment management landscape.

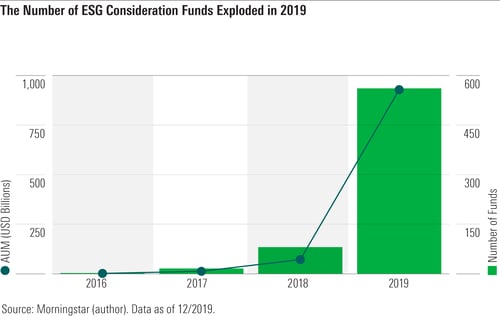

To meet the increased demand from clients, the industry responded with record numbers of mutual fund and ETF product launches in 2019. A jump in AUM from 2018 was met with an explosion of ESG funds that were either launched or repurposed during the following year. The commitment by industry heavyweights like BlackRock, State Street Global Advisors, Goldman Sachs, and many others was a clear indication that ESG investing had dispelled my earlier belief that it would never become mainstream.

This phenomenon has important implications for retail investors who are interested in socially conscious investing but are not interested in picking individual stocks. For example, a friend of mine came to me recently with a simple request to build a portfolio of investments that are “doing the right thing” in the world. This exercise is much easier today, as Main Street investors have a variety of mutual funds and ETFs to choose from when constructing portfolios, which was not the case five years ago.

A diversified opportunity

My second misconception about socially conscious investing was that it would be challenging to deliver superior performance over time. This rationale centered around the notion that the universe of securities that were considered by ESG funds was too limited. I believed that having a smaller “pool” of stocks to choose from would handcuff portfolio managers in their quest to outperform traditional portfolios that had an unlimited universe of available securities to consider.

My rationale may have been applicable in the early days of socially conscious investing, when many of the investment products were mainly focused on companies that were deemed to be environmentally friendly. But the evolution of ESG investing to include an emphasis on corporate governance has resulted in broader investment mandates that offer an opportunity for more diversified exposure. Today, many of the ESG-oriented investment products have representation across nearly all sectors of the market; thus, the opportunity for outperformance is, in theory, better today than it was five years ago.

A record of outperformance

Companies that rank favorably from a corporate governance perspective are generally those that are deemed to be higher “quality.” These companies are typically run in a more prudent fashion when it comes to how they manage their balance sheets and how they reward their various stakeholders. In my opinion, higher-quality companies have shown a tendency to outperform over time and, in particular, during periods of market weakness.

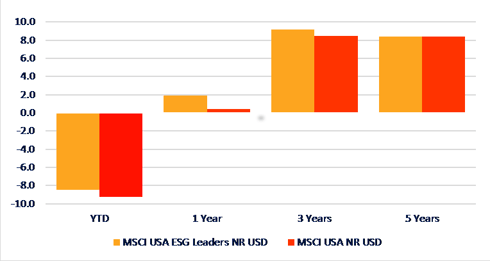

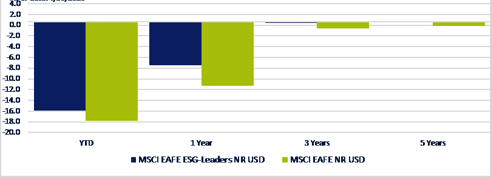

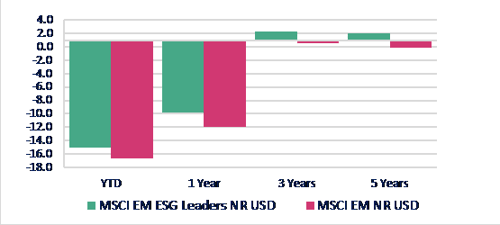

Looking at the relative performance of ESG mandates seems to validate this conclusion across a variety of markets. Below are a series of charts that show the performance of ESG indices from MSCI compared with their traditional benchmarks. The performance of the past five years makes a pretty compelling argument against the notion that ESG strategies are handcuffed in any way. The data was particularly eye opening in emerging markets, as the MSCI Emerging Markets ESG Leaders Index was able to deliver more than 2 percent of annualized outperformance over the past five years.

Returns (as of April 30, 2020)

Source: Morningstar Direct

Returns (as of April 30, 2020)

Source: Morningstar Direct

Returns (as of April 30, 2020)

Source: Morningstar Direct

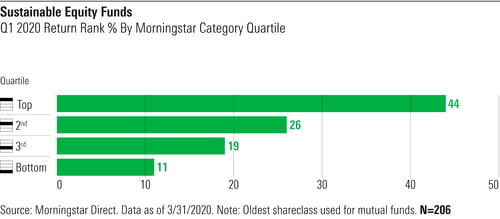

The outperformance of ESG mandates compared with traditional indices has been noteworthy, but how have they done relative to their peers? In particular, how well did they hold up in a difficult market environment such as the one we experienced in the first quarter of this year? It turns out that the higher-quality bias of these mandates has been helpful in protecting on the downside. As the chart below illustrates, 70 percent of sustainable equity funds delivered above median performance during the sell-off in the first quarter of 2020.

A better way to invest?

When I began my career as an investment analyst, I was skeptical of most anything and everything. I’d like to think I’m a bit wiser today, and I’ve come to realize that my skepticism related to ESG investing was misplaced. Asset flows are likely to continue their recent trend as more and more people come to understand that ESG investing is about much more than feeling good about the companies they own in their portfolios. Quite simply, it may just be a better way to invest.