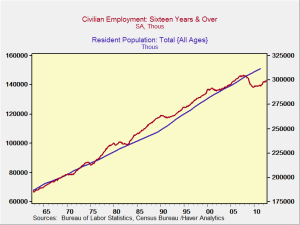

To try to estimate where the real economy will be in 2013, we must first consider where growth might come from. Consumer spending is approximately 70 percent of the economy, so this will be the first area we consider.

December 19, 2012

To try to estimate where the real economy will be in 2013, we must first consider where growth might come from. Consumer spending is approximately 70 percent of the economy, so this will be the first area we consider.

December 18, 2012

In the fiscal cliff debate, both sides have started to take off the gloves and trade offers. Boehner threw in the first bid, offering to accept higher rates on incomes over $1 million, and Obama said that he might be willing to move the bar above the $250,000 he’d been holding at. Obama’s most recent bid is for a $400,000 threshold. So we’re getting much closer.

On spending cuts, there’s been less progress. The President has ignored a Republican proposal to increase the Medicare eligibility age to 67. Not no progress, though, as Obama did accept a GOP proposal to use a different inflation formula for benefit calculation. This is important because it will result in big cost reductions (and benefit reductions) over time.

December 18, 2012

At the end of 2012, the U.S. economy finds itself, almost, at the beginning of a sustainable recovery. Consumer spending has recovered to levels above previous highs and is on par with recoveries from previous recessions. Retail sales are also doing well. The housing market has turned, with most markets reporting price increases year-on-year, and the number of houses for sale in most markets is below historical averages, suggesting that price appreciation will continue.

December 17, 2012

— Guest post from Peter Essele, senior investment research analyst

One area of the economy that has been making a strong comeback as of late is the housing market. During the depths of the recession, housing was among the most undervalued areas of the investable spectrum, as affordability reached multidecade highs. Countless valuation metrics, including price-to-rent and price-to-median income ratios, moved well beyond the averages witnessed over previous decades. The mindset of investors toward housing went from viewing it as an asset class that never depreciates to believing that it would never recover—all in a matter of years.

December 17, 2012

That’s an unfair headline, but what the heck. The big political and economic news in the U.S. this weekend was Speaker Boehner’s offer to allow higher tax rates on those making more than $1 million per year. That at least was the headline. But buried in the proposal was something more significant—an offer to extend the debt ceiling for at least another year or so.

The GOP—at least the portion of it not in safe, gerrymandered districts—is starting to recognize that, if the country does go off the cliff, the Democrats will get a lot of what their base wants—higher taxes, especially on the “rich,” and lower military spending—and the Republicans will get blamed by the Independents. Sure the country will suffer, but from a political point of view it doesn’t get much better than that for the Democrats. Boehner, who is speaking for the wing of the GOP that will be exposed in the next election cycle, is trying to cut a deal—or at least look as if he is doing so. As predicted, this is coming at the last minute.

Probably the best description of a movie I’ve ever read was of Independence Day, a great science fiction B movie. (If you haven’t seen it and you like that sort of thing, take a look.) The description goes, “Space aliens come and destroy Washington, D.C. But later on, it turns out they are hostile.”

I think of that every time I look at the performance of the economy, which is recovering, and then read the headlines about the fiscal cliff negotiations, or lack thereof. There are certainly risks out there that could derail the recovery, but it’s maddening that the biggest one is our own government.

December 13, 2012

So the big story today is that the Federal Reserve is now explicitly linking its interest rates to U.S. unemployment. It’s kind of the reverse of the Santa revelation. Remember when you found out that Santa wasn’t real? How you kind of knew it but weren’t happy to have it confirmed? Now we kind of knew that the Fed was keying on unemployment, but again we’re not all that happy to have it confirmed.

The story made the front pages of the Financial Times, the Wall Street Journal, and the New York Times, in all cases above the fold. So in the eyes of the mainstream—and especially the financial—media, this is a big deal. I agree, for a change. The Fed has explicitly moved toward supporting the real economy, in employment, and away from supporting the financial economy, with inflation. Clearly, it is worried more about the former than the latter.

December 12, 2012

The primary story today is the imposition of restrictions on unions in Michigan, home of the United Auto Workers and once seen as a mainstay of the union movement. This news hit the front pages of the Wall Street Journal, with “Unions Dealt Blow in UAW’s Home State,” and the New York Times, with “Limits on Unions Pass in Michigan, Once a Mainstay.”

The story is important for the obvious reasons, such as the continuing erosion of worker power, but it is also important for some less obvious ones. Among these is that the erosion of wage bargaining power makes general price inflation less likely. A key driver of the out-of-control inflation in the U.S. during the 1970s was the wage-price spiral. At the time, wages were indexed to increase with prices, largely through union contracts, and the two fed each other in an increasing spiral. Today, as the membership and power of unions erode, wage-price inflation is becoming less of a worry for the economy as a whole.

December 11, 2012

Just a quick note regarding some of the more interesting things I have read recently.

December 11, 2012

I have spent quite a bit of time reading, thinking, and writing about the fiscal cliff, going into its potential risks and damage in some depth. While it’s certainly appropriate to analyze the situation, something occurred to me the other day: Could this be another Y2K?

You may remember it—the disaster that didn’t happen. Despite the predictions of nuclear power stations melting down and airliners dropping from the sky, the millennial New Year celebrations went just fine, and the world was still there the next day.

{kind=link}