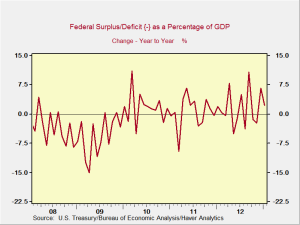

The deficit has dropped off the radar for a bit, what with the agreement to postpone debate about the debt ceiling and the generally improving economy, but recent events make it a good idea to check in and see where we are.

April 30, 2013

The deficit has dropped off the radar for a bit, what with the agreement to postpone debate about the debt ceiling and the generally improving economy, but recent events make it a good idea to check in and see where we are.

April 29, 2013

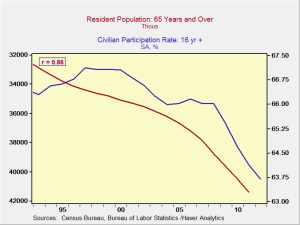

Over the past year, I’ve written about a number of issues that touch on demography, explicitly invoking it in discussions of employment and future growth. Like the group of blind men examining the elephant, however, I haven’t really considered the thing as a whole.

Demography, the study of the structure and characteristics of human populations, is almost unique in the economic universe in being something we can forecast with a great degree of certainty. We know, for example, how many people were born in 1965—that won’t change once the year is over—and we have a very good estimate of how many have died or had children since then. Unlike, say, employment, demography evolves over decades in a predictable way.

April 26, 2013

We’ve been talking about how the U.S. real economy, despite a second-quarter slowdown, continues to grow. The Fed by and large agrees, with several governors weighing in over the past couple of weeks to say that they see a sustainable recovery in place and that it’s time to start thinking about when and how to begin pulling back. You might be forgiven for thinking “Hooray!” After all, isn’t sustainable growth what we’ve been working toward for the past five years?

Although we do seem to have sustainable growth from multiple sources—housing, autos, and energy, among others—much of that growth is driven by current low interest rates, especially in housing. When the Fed starts pulling back, there is a reasonable possibility of higher interest rates, which will at least slow that growth.

April 25, 2013

Several data points have come through in the past couple of days that support some thoughts I’ve had for a while. I think it’s constructive to take a look at them to determine how we can expect the economy and financial markets to evolve in the near future.

April 24, 2013

Is it possible to predict the stock market? As usual, it depends on what you mean. If you mean determining where the market will close today or tomorrow, or what a particular stock will do next week, the answer is no. It’s when you get into longer time frames, or larger portfolios, that things get interesting.

It also depends on what you mean by “predicting.” Are you, for example, looking at calling an exact number or just seeking an idea of likely outcomes? If the former, you’re out of luck; if the latter, you can probably make some headway.

April 23, 2013

Yesterday, we talked about how the opportunity cost of not spending on defense might in the end be greater than the spending. Today, I’d like to do the same for social security.

I don’t believe the case for spending is clear here, and I’m mindful of the weakness in the opportunity cost argument. After all, if I bought all of the great deals I get in my e-mail every day, I would be bankrupted by the savings. But that’s a different post.

April 22, 2013

I was in Virginia late last week, speaking to a group of clients, and had a couple of interesting conversations that are worth expanding on here. To start off, we talked about what the U.S. is actually spending its money on, and how and whether it made sense to cut. This is a slightly different take on the spending discussion than you normally see. Typically, the discussion is based on the assumption that spending is more or less set; the issue is how to cut, rather than whether cuts make sense.

April 19, 2013

I am in Virginia today and tomorrow, speaking to groups of clients. With no major economic stories going on, I thought I would do a couple of quick hits on various topics.

April 18, 2013

As I wrote after Cyprus, I moved from a not-at-all-certain belief that the euro would make it, for political reasons, to a just-as-uncertain suspicion that it would not (also for political reasons). Recent events continue to widen the gap between the “make it” and “not make it” conclusions.

When Greece first defaulted, the narrative was all about irresponsible Greek borrowing, with the clear implication that they had it coming. News coverage focused on early retirement, state pensions at 50, and low tax compliance. In fact, when default hit, imports of necessary goods such as medicines also essentially stopped for most of the population. Very little of that made it into mainstream coverage.

April 17, 2013

On the heels of yesterday’s post on risk, outliers, and uncertainty, I saw an interesting article today in the New York Times. It discusses a recent paper highlighting potential errors in the work of Carmen Reinhart and Kenneth Rogoff, authors of the influential 2010 economic study “Growth in a Time of Debt” and the book This Time Is Different.

Covering financial crises in many countries over the past several centuries, Reinhart and Rogoff’s (RR) massive study draws the conclusion—controversial in certain circles—that, when a country’s overall debt exceeds a certain level with respect to the size of the country’s economy, expressed as GDP, future growth declines. It is used as an argument against excessive government spending and debt, particularly here in the U.S.