Today’s topic is a particularly good and timely question from a reader:

“Why would economic problems in other countries, especially smaller, emerging markets, cause a drop in the U.S. equities market?”

February 20, 2014

Today’s topic is a particularly good and timely question from a reader:

“Why would economic problems in other countries, especially smaller, emerging markets, cause a drop in the U.S. equities market?”

February 19, 2014

We have two interesting things to look at today: a report from the Congressional Budget Office on the effects of a higher minimum wage, and a report that consumer borrowing has ticked up as banks become more willing to lend.

February 18, 2014

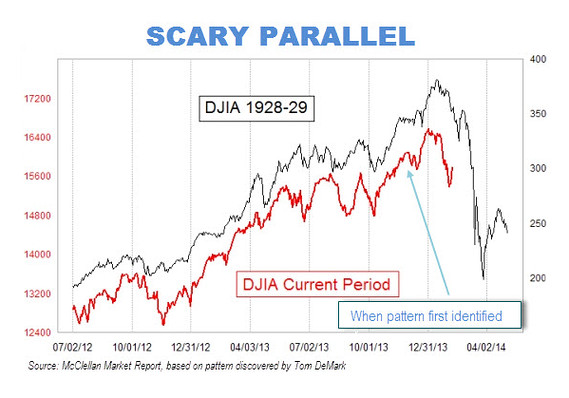

I’ve been getting more “disaster chic” questions recently, and I thought I’d get ahead of what I expect will be the next driver of such concerns. Over the weekend, Mark Hulbert wrote a column about a scary chart that’s making the rounds, showing very real similarities between the way the market behaved before the crash in 1929 and right now.

February 14, 2014

First, a shout-out to my wife, Nora, who’s been stuck with the snow for the past two weeks while I’ve been traveling. She’s done a lot of work and a great job, and I am extremely grateful. Happy Valentine’s Day, sweetheart!

The bad weather has actually been an occasion for good karma. I’ve spent quite a bit of time over the past couple of years helping neighbors clear snow; it’s just the right thing to do for a lot of reasons. Yesterday, while waiting at the airport, I got a delighted text from Nora that someone had plowed our driveway, and when she and Jackson got home, the job was largely done. That was a wonderful surprise. Karma works, although sometimes it can take a while.

February 13, 2014

I have written before about the work of Professor Robert Gordon and others, who are projecting much lower growth in the next hundred years than in the past. The rationale, briefly, is that all of the easy gains have been taken. The world will not be electrified again. Agriculture has already been largely mechanized. Labor-saving inventions, like the washing machine, have already fully penetrated the developed nations and are working their way through the emerging markets. At some point in the not-too-distant future, it will be possible to satisfy people’s material needs fully.

With population growth topping out, as it is, and with material needs on their way to being addressed, will growth even be necessary? Imagine a world with a stable population, where everyone has enough material goods—what growth would we need? What would growth even mean in that context? Even if Gordon was right, would it matter?

February 11, 2014

When Janet Yellen testifies to Congress for the first time as chair of the Federal Reserve, she will have a very unusual second chance to make a first impression.

February 10, 2014

One of the more interesting ads in a generally disappointing Super Bowl—I know I wasn’t the only one looking forward to a much more exciting confrontation between the number-one offense and the number-one defense—was the puppet-maker who supposedly quit her job on national TV. I have to say, if it was real, it took guts. If the new business doesn’t work out, she may have a hard time going back.

February 7, 2014

With regard to the title, I am aware of the rule that says never end a sentence with a preposition. But I stand with no less an authority than Winston Churchill in saying that this is the sort of nonsense rule up with which I shall not put. So there.

February 6, 2014

It is hard to think of two companies that are more different than General Motors and Twitter. One deals in heavy metal, is both an American industrial titan and an icon of business history, is a recovering bankrupt, and is everything to do with manufacturing real assets that last a long time. The other is a new company that deals in the deliberately short and ephemeral, employs relatively few—especially when compared with GM—and is a titan of the new social media era. The fact that both are actually successful American businesses gives a look at the scope of what our economy actually covers.

And, yet, even given their diversity and scope, these companies do have something in common—both have seen their growth prospects come into question, as previous assumptions of strength are proving false.

February 5, 2014

Recently, the weather has been blamed for poor employment figures, poor car sales, and pretty much every other lackluster economic result. Is this a legitimate explanation or just an excuse?

{kind=link}