Print

Print What a whirlwind year it has been in the financial markets. Not since 1994 have investors seen simultaneous declines in both equities and fixed income, prompting many to question the viability of holding both in a portfolio context. Negative performance across asset classes during the first half of 2022 challenged even the most ardent believers of diversification and modern portfolio theory, leaving many of us to wonder whether we are entering a new paradigm for asset allocation. Should investors abandon the view that stocks and bonds can provide complementary exposures in a portfolio? Disclaimer: I don’t think so.

What a whirlwind year it has been in the financial markets. Not since 1994 have investors seen simultaneous declines in both equities and fixed income, prompting many to question the viability of holding both in a portfolio context. Negative performance across asset classes during the first half of 2022 challenged even the most ardent believers of diversification and modern portfolio theory, leaving many of us to wonder whether we are entering a new paradigm for asset allocation. Should investors abandon the view that stocks and bonds can provide complementary exposures in a portfolio? Disclaimer: I don’t think so.

First Stop: Fixed Income

Much of investors’ consternation as of late has to do with the fact that bond prices have fallen dramatically in the face of an abrupt increase in interest rates. In some ways, this sentiment is understandable given the significant inflationary pressures present in the global economy, coupled with the fact that interest rates were previously at historically low levels. Simply put, inflation has wreaked havoc on consumers and investors alike. Whether filling up your gas tank or looking at the performance of a core bond mutual fund, the first six months of 2022 entailed noticeable inflation effects.

Yet it might be reasonable to believe that the worst is behind us, in terms of rising yields and falling bond prices. The forecast for falling inflation in the second half of the year should bode well for longer-term interest rates—a dynamic that we are already starting to see play out in bond markets. As shown in the chart below, the yield on the 10-year U.S. Treasury is well off its highs of around 3.5 percent over the past couple of months.

Source: FactSet

Another notable takeaway from this chart is the drastic increase in yields, especially over such a short time. While there is the risk we could witness a similar move again this year, I don’t believe there is a high probability of that scenario occurring, especially as economic data softens and inflation data moderates over the coming months. My view is that longer-term interest rates will be rangebound for a period of time, and it is unlikely that previous yield levels (lows or highs) will be revisited any time soon.

Should longer-term interest rates remain near current levels, balanced investors may want to consider the opportunity that rising interest rates present: the ability to reinvest coupon payments at higher yields. The additional income that is earned from reinvesting at higher yields can serve as a tailwind for portfolio returns over the long term. Plus, in an actively managed individual bond portfolio, there may be opportunities to purchase bonds below par—which, if held to maturity, should allow for capital appreciation in addition to higher coupon income.

Next Stop: Asset Allocation

Despite facing many abnormalities this year, the broader asset allocation conundrum is not solely confined to determining the “right” mix of equity and fixed income. For example, within an equity allocation, there are many different asset classes that are expected to deliver diversification benefits, while also performing differently in various market environments. While one asset class zigs, another typically zags, and vice versa. Ultimately, this ability to combine asset classes with lower correlations can help mitigate volatility and help reduce a portfolio’s overall risk profile over the long run.

But during a challenging year such as 2022, asset classes experienced higher-than-normal correlations. Look no further than equities and fixed income, which declined in concert for the first four months of the year. Bonds were unable to provide the historical hedge for equity markets as traditionally seen with fixed income’s ability to provide a ballast during periods of equity market volatility in the past. In fact, bonds experienced one of the worst sell-offs in bond market history, exacerbated by the Fed’s aggressive monetary policy to combat inflation.

So, what can we learn from the synchronous performance of bonds and equities this year—and what does it mean for investors going forward?

A Mixed Bag

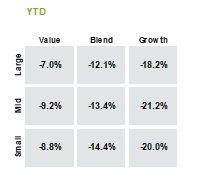

First, let’s start with the bad news. All equity asset classes have posted negative returns so far this year, as the effects of higher inflation, the war in Ukraine, and stretched valuations have resulted in stocks entering bear market territory in June 2022. Year-to-date returns across all equity sizes and styles remain in negative territory, as illustrated below.

Source: JPMorgan Guide to the Markets (as of July 31, 2022)

But there’s also some good news. As the old saying goes, periods of dislocation present opportunities. As of late, we’ve seen disparate returns across equity style boxes, a promising sign for asset allocators. Perhaps the most notable example is the ever-evolving dynamic between growth and value. After witnessing several years of growth’s outperformance, value stocks have gained more than 1,000 bps of outperformance across large, mid, and small caps. While it may not seem like an ideal scenario to be down 7 percent in large-cap value, mitigating the downside and preserving capital during difficult market environments are critical when building long-term wealth.

Value’s recent outperformance over growth has been mildly reminiscent of the beginning of my investment career in 1999. It was the height of the dot-com era. Value stocks had fallen out of favor, and investors were chasing growth. Then the bubble burst—the Nasdaq lost more than 75 percent from March 2000 to October 2002. Meanwhile, the Russell 2000 Small Cap Value Index delivered a positive return during that same time period.

A Valuable Lesson for Investors

While this is one of the more extreme examples of asset class diversification, it still remains a valuable lesson for investors today. Ultimately, it is important to take a view and appropriately tilt portfolios toward areas of equity and fixed income markets that you consider attractive. But avoiding too much concentration risk by allocating toward all asset classes can help investors expand their opportunity sets and participate in various market environments. Despite facing the aforementioned headwinds this year, a well-diversified portfolio can help investors limit losses during periods of market volatility, prepare for the next inevitable unknown, and help improve risk-adjusted returns over the long term.