Print

Print Anu Gaggar, our international analyst, is from India and regularly goes home to visit. I am excited to share her eyewitness, informed report on what is going on there. At Commonwealth’s National Conference, I highlighted the potential opportunities in India. Here, Anu makes very clear that the opportunities are real—as are the risks. Take it away, Anu!

Anu Gaggar, our international analyst, is from India and regularly goes home to visit. I am excited to share her eyewitness, informed report on what is going on there. At Commonwealth’s National Conference, I highlighted the potential opportunities in India. Here, Anu makes very clear that the opportunities are real—as are the risks. Take it away, Anu!

Thank you, Brad, for the chance to share my observations. I recently returned from my biannual visit to India. I always look forward to these trips, not just because I get to see a sea of family (no pun intended) but also because I get to bring back a boots-on-the-ground report. During my last visit two years ago, I witnessed firsthand the announcement of demonetization by the Indian prime minister and the chaos it created in its immediate aftermath. This time, my visit coincided with another significant event—the resignation of the governor of India’s central bank (Reserve Bank of India) amid speculation of mounting government pressure on the bank.

A politically charged country

India, like most other democracies, is a very politically charged country. Everyone appears to have a view on how the country should be run and the shortcomings (or strengths) of the current administration. I was curious to learn people’s views on the Modi administration, especially as India is heading into general elections in two months.

Under the current administration, there have been many reforms in India, primarily the goods and services tax (GST), the Insolvency and Bankruptcy Code (IBC), and demonetization. There was certainly no consensus view on the success of any of these reforms. The GST appeared to have the most impact on the business community, particularly on small, unorganized businesses. It has reduced the scope for tax evasion and, understandably, has had a negative impact on the near-term competitiveness of small businesses.

The effects of the these reforms, along with concerns about an uncertain political landscape and slowing global growth, resulted in corporate investments in new projects sliding to a 13-year low in the fourth quarter of 2018. The departure of the Reserve Bank governor had a negative effect on investor sentiment as well, as it appeared to be in defiance of the government’s attempt to exert greater influence on monetary policy.

The verdict is still out on how these reforms will shape the upcoming elections. But India’s politics, in aggregate, are increasingly focused on economic performance. Hence, irrespective of the political regime, reforms will continue to progress, albeit at different speeds.

Infrastructure changes gaining momentum

India is the second most populous country in the world. Reforming a country of this size, with its multitude of political parties and an unwieldy bureaucracy, is no small feat. Not surprisingly, translating policy measures from paper to action has been a very slow-moving process in India. I did notice that the scale and pace of activity have gathered momentum. Every major town and city I went to (nearly 10) was undergoing major infrastructure build-out. This work, of course, made traveling a nightmare but also raised my hopes that my next visit will be much more pleasant.

A digital revolution

Technological advances are rapidly revolutionizing India’s economy. Nearly 500 million people are online in India, even as basic Internet service has not yet reached 70 percent of India’s population. The scale and potential are massive and will likely enable India to leapfrog a generation of older technologies. Everywhere I went, I observed people glued to their smartphones (which I wasn’t too excited about!). From a business standpoint, however, this digital revolution could present tremendous growth opportunities. There is an increasing proliferation of Internet-only companies with no brick-and-mortar presence. Digital transactions are growing more rapidly than cash transactions. Global integration is occurring at a fast clip, with increased awareness and access to global brands.

Demographic dividend or disaster?

One change that I observed everywhere I went was the increasing affordability and appetite for consumption. This reality is quite different from my experiences growing up, when purse strings were tight and discretionary spending was frowned upon. I also noticed a widening gap between the haves and have-nots. Much is made of India’s demographic dividend, whereas much of the developed world is aging. It is estimated that by 2020, the average Indian will be only 29 years of age, compared with 37 years in China and the U.S., 45 years in Western Europe, and 48 years in Japan. This statistic undoubtedly excites many consumer-oriented companies, as well as companies looking for a new home for their operations should trade talks with China disintegrate.

In the long term, economic growth is a function of the total number of workers and their average productivity. Although the number of workers in India is growing, labor productivity in the country is near stagnant. Sadly, more than 90 percent of the country’s workforce is unskilled or low skilled, and most are employed by the informal sector where productivity and wages are low. Moreover, the number of unemployed people is increasing every day. Thus, if the incumbent government does not undertake widespread measures to address the skills deficit, reform the archaic labor laws, increase participation of women in the workforce, and enhance ease of doing business for small and medium enterprises, the demographic dividend could easily turn into a demographic disaster.

A land of opportunities

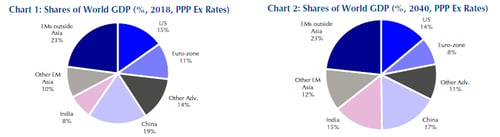

I am happy to report that India is indeed a land of opportunities for the medium to long term. It is currently going through the growing pains of an emerging economy. But increased penetration, formalization of the economy, high savings and investment rates, and rapid digitalization will help sustain high economic growth rates for a long time. In fact, according to Capital Economics estimates, the Indian economy will triple in size in the next two decades, and its share of world GDP will increase from 8 percent to 16 percent. This is certainly a size that will not go unnoticed.

Source: Capital Economics

As you can imagine, I am already excited for my next visit to India. For now, I look forward to reporting on the upcoming “spectacle” that the largest democratic exercise in world history promises to be when more that 850 million voters decide the political fate of their country.