Print

PrintI speak regularly to groups of advisors and clients, and a question that has come up several times recently is whether the housing recovery can survive rising interest rates. In other words, as rates rise, will we see average housing prices level off or even start to decline again?

The question is becoming increasingly relevant: Mortgage applications have fallen in some weeks recently as rates have risen, and the average mortgage rate just ticked above 4 percent for the first time in quite a while.

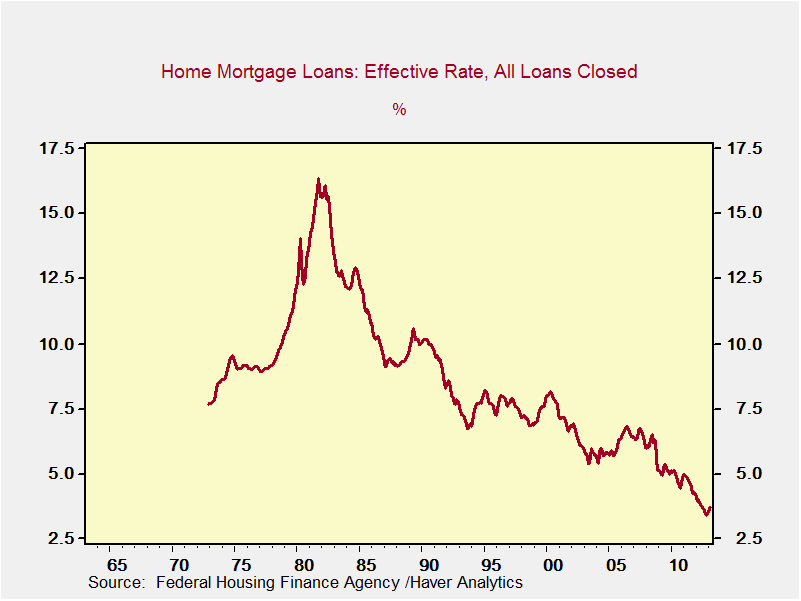

To keep things in perspective, rates are still at almost their lowest levels since records have been kept, per the chart below; they’ve just ticked up a bit. Still, perception is reality, and buyers look at rates in the context of their recent experience. It’s conceivable that this could negatively affect demand.

At the end of the day, the future of housing, like any economic decision, will depend on the market, on the supply and demand for housing. Let’s look at demand first, for without the demand, the supply is irrelevant.

When we consider demand, we have to look at effective demand—that is, demand from people who can afford to act. One way to analyze effective demand is to look at median incomes, to determine how much people can afford to pay. We can then look at current mortgage rates and possible changes to determine how increases in rates will impact effective buying power. From there, we can compare the effective buying power with median home prices to see whether the change in rates changes effective demand given current pricing.

Let’s assume a two-income family, with both husband and wife employed full time. The most recent data from the Bureau of Labor Statistics has median weekly income for men at $867 and women at $704. This equates to a combined income of $1,571 per week, $6,808 per month, and $81,692 per year. Based on a typical ratio of 28 percent, the family could afford to pay $1,906 per month on their mortgage. It’s a bit more complicated than that, of course, but this is a reasonable approximation.

With this payment, assuming a typical 30-year mortgage and a 20-percent down payment, the family could support the following mortgages and home purchase prices. You can see that higher rates do indeed affect the affordability of a home.

Rate Mortgage Purchase Price

3.5% $420,000 $525,000

4.0% $400,000 $500,000

4.5% $376,000 $470,000

5.0% $355,000 $443,000

5.5% $335,000 $418,000

6.0% $318,000 $397,000

The first thing I would note about these calculations is that no one in his right mind would actually borrow this much—these numbers represent what a borrower could qualify for, not what he should actually do. Nonetheless, they do provide a guide to affordability overall.

The median price of a single-family home, depending on which data set you look at, is around $200,000, which is a nice round number. Looking at the figures above, we see that, even at a rate of 6 percent—well above current rates—affordability for the average family doesn’t look to be a problem.

Even if we take a more restrictive look—using after-tax income, for example—we still find housing affordable at much higher rates. A 35-percent effective tax rate, which is quite conservative, would give the family an allowed monthly mortgage payment of $1,239, which would lead to the following numbers:

Rate Mortgage Purchase Price

3.5% $275,000 $343,000

4.0% $259,000 $323,000

4.5% $244,000 $305,000

5.0% $230,000 $287,000

5.5% $218,000 $272,000

6.0% $206,000 $257,000

Using this more conservative approach, the median-priced house remains easily affordable, even at much higher interest rates.

Another way to look at demand, though, is to compare the relative costs of buying and renting. After all, just because a family can afford to buy doesn’t mean they will. What if it’s cheaper to rent? Comparing the costs of renting versus owning isn’t simple, in that I have numbers for the median apartment rental rate in the U.S. ranging between $801 and $1,430 from various sources. For purposes of argument, let’s use the U.S. Census figure from 2011 for units built in the past four years, or $1,052. (Given rent increases since then, the number is probably higher, but it should be close enough.)

Given a 20-percent down payment and the median house price of $200,000, the monthly mortgage costs are as follows:

Rate Mortgage Payment

3.5% $160,000 $719

4.0% $160,000 $764

4.5% $160,000 $811

5.0% $160,000 $859

5.5% $160,000 $909

6.0% $160,000 $960

Even at the lowest average rent figure, a mortgage payment is less than rent using current interest rates. For the Census rent figure, mortgage payments would be less than rent even at rates well above 6 percent.

This is obviously a simplified analysis. I am ignoring real estate taxes and maintenance costs, but I’m also ignoring the mortgage interest tax deduction. I am ignoring the freedom to move that comes with renting, but I’m also ignoring the value of locking down housing costs into the indefinite future. Rents can go up; fixed mortgage payments don’t. Furthermore, I am ignoring the psychic benefits of home ownership, which haven’t gone away and, even when renting was cheaper, continued to drive people to buy.

The biggest thing I’m ignoring, however, is the down payment. Why? Except for the period from 2005 to 2007 or so, the down payment has always been necessary. The need for a down payment isn’t a new factor—rather, it represents current conditions—and we don’t need to model a change in this analysis.

Taking all of this into account, buying demand for homes doesn’t seem likely to be crippled by higher rates, at least in the immediate future. Given a down payment, it’s now cheaper to buy on a median basis and will continue to be so for some time—with all of the other benefits of home ownership thrown in for free. Considering the amount of pent-up demand out there and the decreasing supply of homes available, it seems more likely than not that both demand and prices will continue to increase even if interest rates keep climbing.