Learn why I told CNBC Worldwide Exchange that I think taking out protection against a deeper correction is a good idea at this point in an interview today, June 25.

June 25, 2014

Learn why I told CNBC Worldwide Exchange that I think taking out protection against a deeper correction is a good idea at this point in an interview today, June 25.

January 13, 2014

Listen to Brad’s interview on MarketWatch, where he discusses the stock market’s behavior in the first weeks of 2014.

January 7, 2014

Every year, I struggle with the notion of preparing an outlook—I won’t use the term forecast—for the following year. Every year, I point out, to no avail, that it would be much better to do a forecast for the previous year: better data, much more context, and certainly greater accuracy. I’ve had no more success this year than usual, so I’m preparing my outlook as you read this.

The reason I call it an outlook, rather than a forecast, is that forecast implies a level of certainty that, even in principle, simply isn’t achievable. I used the simile the other day that the Fed’s job is like trying to repair a Seiko watch based on a Timex manual, using a sledgehammer operated by a robot controlled from the next room, in the dark, and I stand by it.

December 31, 2013

2013 is over. There was a lot of good (have you looked at the stock market?) and a lot of bad (think Washington, DC). There were lots of highs—the stock market again—and lows, such as the EU’s decision to hit Cyprus depositors. Overall, it was a pretty typical year in many respects, although of course we get different highs and lows every year.

2014 will be different. 2013 started with angst and a broken budget; 2014 starts with a smoothly negotiated (if rather minimal) budget deal. 2013 started with worry about fiscal collapse and an exploding deficit; 2014 starts with the deficit projected to decline to below the growth rate of the economy. 2013 started with zero growth; 2014 starts with the most recent quarterly growth figures above 4 percent.

December 24, 2013

I have always loved Christmas. But as I grew older, as much as I loved it, I think I lost much of the spirit. Now that I have a four-year-old son—who is wrestling with the stress of being good under the eye of the “Elf on the Shelf,” eying presents under the tree, and baking cookies with his mom—I find myself recovering much of what I had lost. This is wonderful, but, as a father, I also find myself reaching deeper into the meaning of the holiday.

The idea of sacrifice is at the heart of both Judaism and Christianity, and the notion of a father sacrificing his son is fundamental. Christmas itself, where the Christ child is born into the world, is the start of just that sacrifice. I literally cannot fathom making that kind of sacrifice—of giving up my son. At the same time, I understand just how much I would sacrifice for him.

After writing about how growth could slow going forward, based on my own analysis and supported by several even more pessimistic analysts, notably Jeremy Grantham and Professor Robert Gordon of Northwestern, I have been spending some time thinking about how the argument is wrong.

December 17, 2013

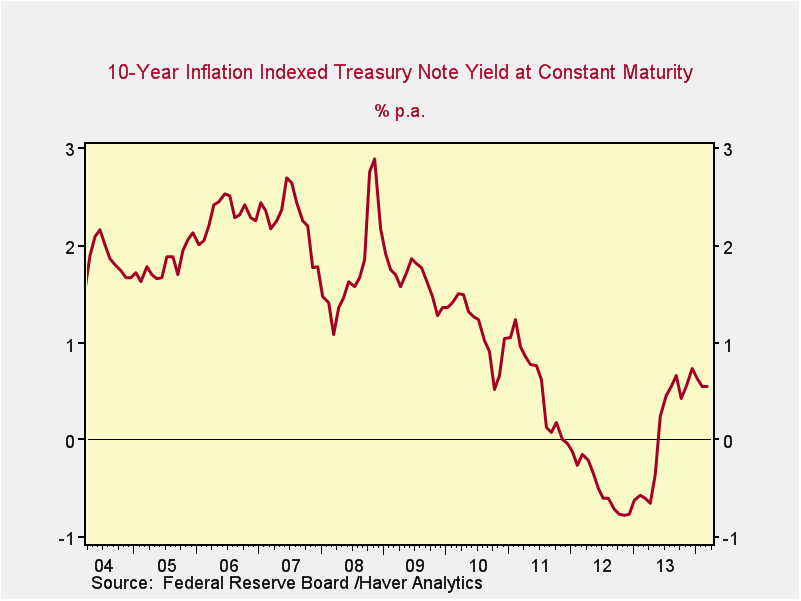

The last time that the Federal Reserve (Fed) was widely expected to start reducing, or “tapering,” its bond purchase program, earlier this fall, interest rates increased and the market tanked. Widely referred to as the “taper tantrum”—a term I wish that I had invented—the drop was quickly reversed when Fed officials came out and reassured the market that, in fact, they had no intentions of pulling back, ever. Really.

That was then. Since that time, the economy has shown improved growth, interest rates have ratcheted back down, and the stock market has recovered and powered up to new highs. With the recent good economic news—much higher levels of GDP growth than expected, higher employment figures and lower unemployment, and very positive business surveys, among other highlights—the Fed is at a point where a taper pretty much has to start soon. Maybe not this week, but soon. The budget deal in Washington also makes a taper more likely because the last reason for the Fed to continue its stimulus was worry about fiscal policy disruption.

December 9, 2013

I’ve been working on gathering my thoughts for the market in 2014. This is a very useful exercise, in that it forces us to really think about what goes into stock prices, what those assumptions should be, and how they interact.

There are three key variables here: the growth rate of the economy as a whole and the level and change in profit margins (which together will determine corporate earnings growth), and the level of price multiples (or how much investors will pay for a given level of earnings). The fourth variable, what happens in Washington, DC, factors in as well, of course, but that’s a subject for another day.